Your Comp Budget Is Already Wrong

The most-asked question in any mid-year compensation review, "am I on budget?", is the wrong question, and answering it produces the wrong decisions. The right question, and the one almost no organizations are asking, is whether the budget still represents the company.

The compensation budget was drafted in October. It was assembled from four inputs — an attrition forecast, a hiring plan, a merit pool assumption, and a market positioning estimate — each of which was a snapshot of conditions that had been moving every month since. By the time anyone asks "am I on budget" at H1 close, every input has drifted. The honest answer is almost always "yes, against a financial document that no longer represents the company."

Mercer's most recent compensation planning survey put last year's actual merit increases at 3.2 percent against a 3.3 percent projection — a modest variance at the headline level that compounds across thousands of individual decisions, each carrying a small departure from the assumptions the budget was built on.

WorldatWork data indicates roughly 60 percent of organizations made mid-course corrections to salary budgets in the most recent cycle. The pattern is consistent enough across surveys to be diagnostic: the budget set in Q4 is a starting point, not an operating manual. Companies that treat it as an operating manual carry the drift into every subsequent compensation decision the budget governs.

The drift is not a small refinement. It compounds across four input categories — attrition, hiring, merit execution, market positioning — each moving on its own clock and producing its own variance. The cumulative variance, by H1, typically displaces the budget from reality by margins large enough to invalidate the planning assumptions underneath the next two quarters of comp decisions.

The on-budget test does not detect this displacement, because the test asks whether the company is matching its plan, not whether the plan is matching the company. Both halves of the question matter. Most organizations are answering only the first.

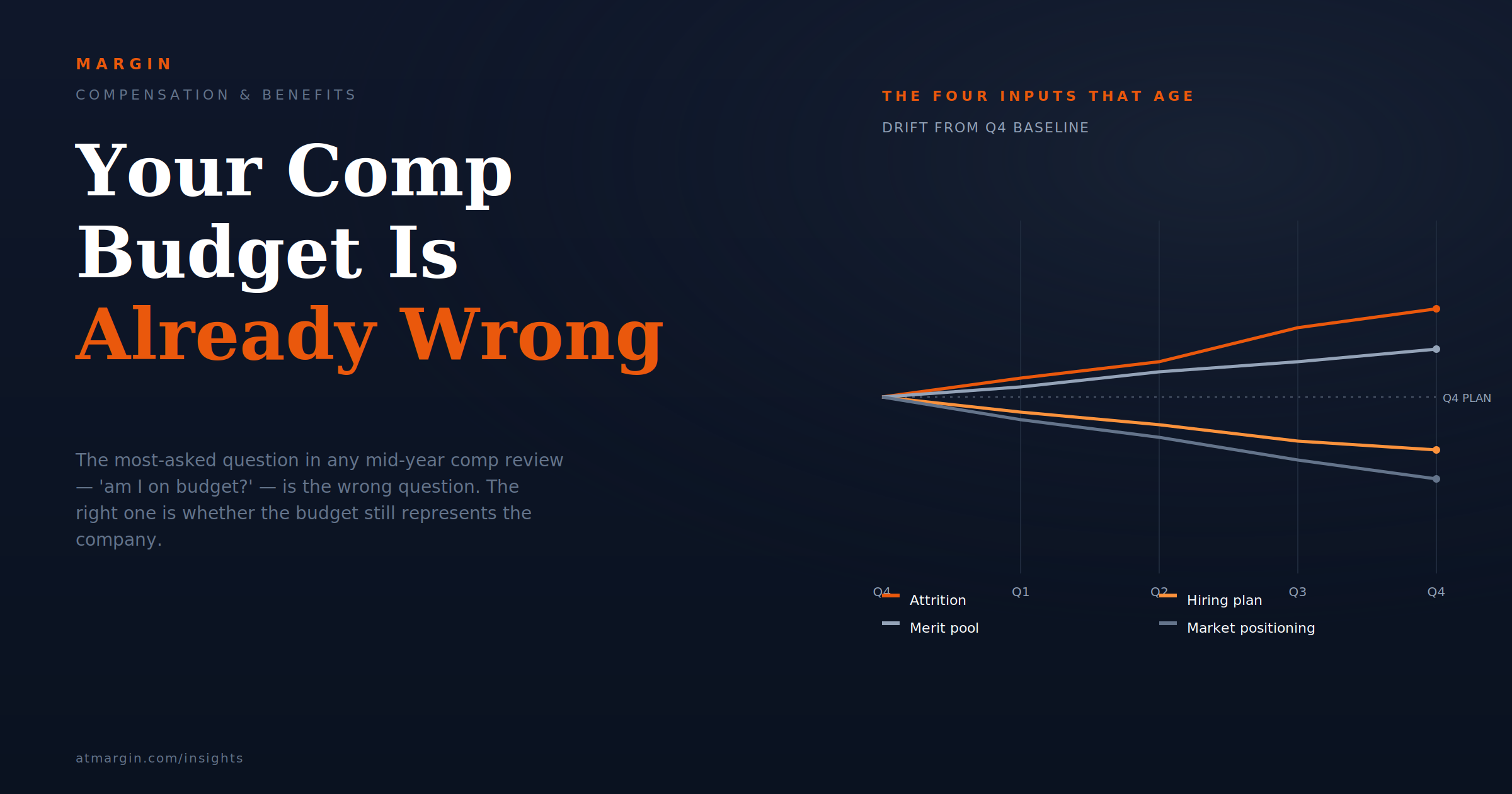

The Four Inputs That Age

A compensation budget is a forecast assembled from four input categories, and each category drifts on a different timeline once the budget is approved.

Attrition

The first input is attrition. The Q4 budget was built on a forecast of voluntary departures by role family and level, with assumed replacement compensation at projected market rates. By H1 close, actual attrition has either undershot or overshot the forecast.

If it overshot — particularly if departures concentrated in higher-paid roles — the unspent salary line creates apparent budget surplus, which most CFOs read as good news. The truer reading is that the budget was overweighted toward retention costs the company didn't have to pay because it lost the people it was budgeted to keep. The "savings" is the cost of lost institutional capacity that the budget never captured.

Hiring

The second input is hiring. The budget assumed a particular cadence of new hires, at particular levels, at particular comp positions within band. By H1, the cadence has shifted — slower, faster, or skewed to different role families than planned. New hires are coming in at compensation positions that reflect current market conditions, which differ from the conditions the budget was built on.

Each new hire whose comp position differs from budget assumption creates a small piece of band drift. By the tenth or twentieth such hire, the pay distribution within the affected role family no longer matches the structure the budget assumes, even when the aggregate spend looks intact.

Merit Pool Execution

The third input is merit pool execution. The budget assumed a merit pool — typically 3.0 to 3.7 percent in 2026 depending on industry, with construction at 3.4 percent, manufacturing at 3.1 percent, and healthcare and retail near 2.9 percent — distributed against an expected performance distribution.

The performance distribution actually delivered will differ. So will manager calibration practices. The 2025 variance between projected and actual merit was modest by the headline number, but the variance compounds across thousands of individual decisions, each embedding a small departure from the budget's assumptions about who gets paid what.

Market Positioning

The fourth input is market positioning. The compensation surveys the budget was built on — Mercer, Pearl Meyer, WTW, Payscale, WorldatWork — refresh on quarterly to annual cadences. Pay transparency mandates have added a near-real-time data stream from publicly posted ranges in sixteen states and counting.

By H1, the formal market data underneath the Q4 budget is six months old; the real-time transparency feeds describe a market that has been moving the entire time. The budget's market positioning — at midpoint, slightly above, slightly below — has drifted relative to a market that has not stopped to honor the assumption.

Each input drifts on its own. Aggregate drift is the cumulative result, and it is rarely linear. A small attrition variance interacting with a small hiring shift interacting with merit calibration drift interacting with market data refresh produces compounding effects that the budget's structure does not capture. By H1, the budget is not just out of date on individual line items. It is operating on a different logic than the company is.

Why "On Budget" Is the Wrong Test

Companies that pass the on-budget test at H1 are not reassured by the result. They should be alarmed by it, because passing the test means one of two things: the inputs didn't drift, or the company didn't notice them drifting.

“On-budget at H1 means one of two things: the inputs didn’t drift, or the company didn’t notice them drifting.”

Inputs always drift. WorldatWork's data placing roughly 60 percent of organizations making mid-course corrections is not a measure of poor planning. It is a measure of intellectually honest organizations.

The other 40 percent are either operating in unusually stable input conditions — rare in 2026 — or running comp on assumptions they have not stress-tested against actual H1 reality.

The on-budget test treats the budget as ground truth and tests the company's adherence to it. Adherence to a stale plan is not a virtue. It is a procedural achievement sometimes correlated with operating discipline and sometimes correlated with the absence of environmental sensing. The two cases are indistinguishable from inside the test. From outside, they produce dramatically different outcomes by year-end.

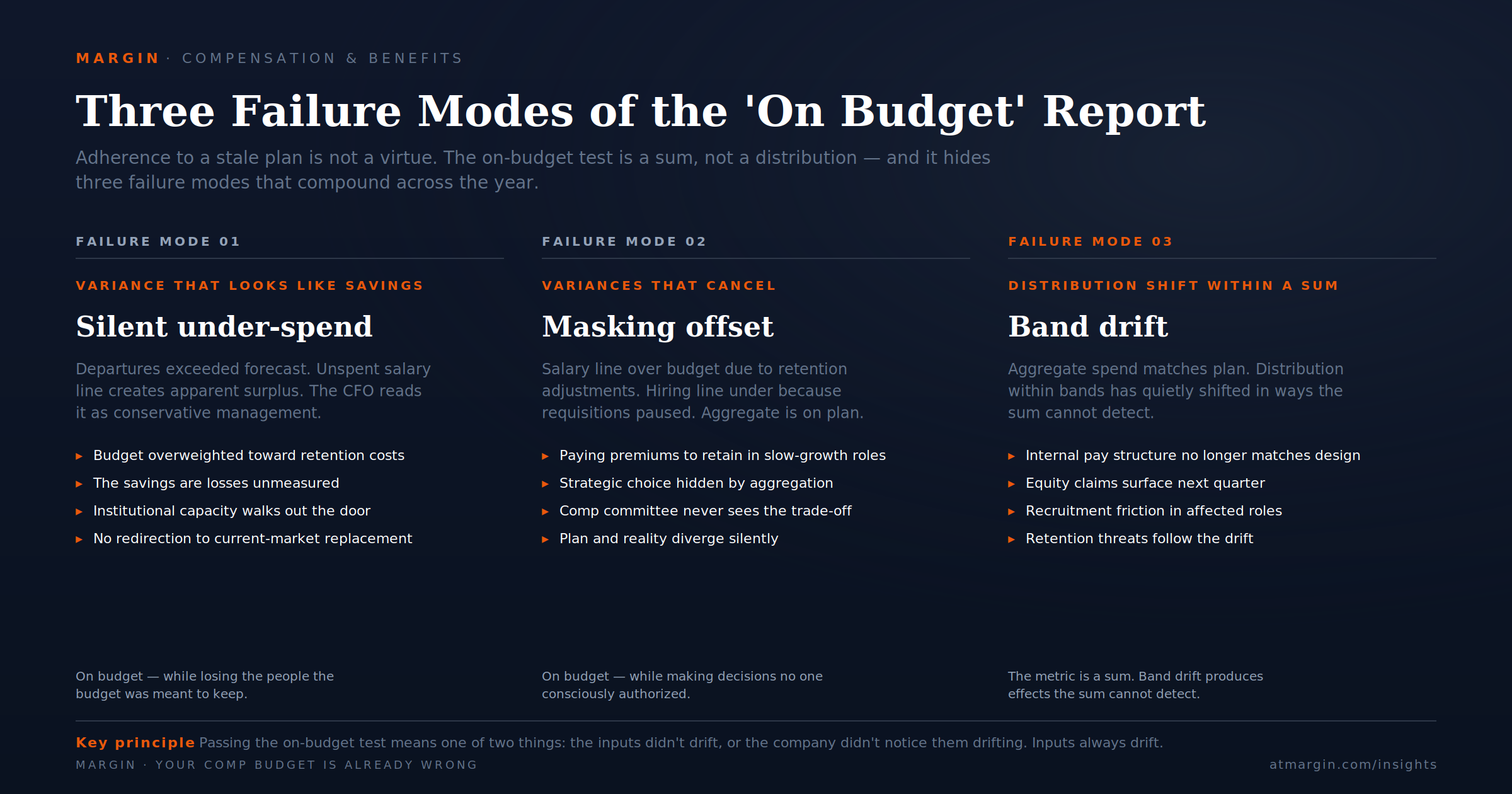

Three failure modes consistently produce on-budget H1 reports that mask serious comp problems.

Silent Under-Spend

The first is the silent under-spend. The company is on budget because departures exceeded forecast and the unspent salary line created surplus. This reads as conservative management. It actually means the comp system failed to retain people the budget assumed would stay, and the savings should be redirected to either replacement hiring at current market rates or to retention investment in the remaining at-risk population.

Companies that don't make this redirection report being on budget while losing the institutional capacity the budget was meant to maintain.

Masking Offset

The second is the masking offset. Two large variances cancel out at the aggregate level. Salary line is over budget because of unanticipated retention adjustments. Hiring line is under budget because requisitions were paused. The aggregate is on plan.

The underlying story is that the company is paying premiums to retain employees in roles it has implicitly decided to grow more slowly, which is rarely the strategic choice the comp committee would make if it were evaluating the situation explicitly. The on-budget number hides the choice.

Aggregate Spend

The third is band drift. Aggregate spend is on budget but the distribution within bands has shifted — new hires entered at higher percentiles than budgeted, off-cycle adjustments concentrated in particular role families, merit dollars allocated unevenly against the calibration plan.

The total payroll number matches the forecast. The internal pay structure no longer matches the company the budget was built on, and the structural mismatch produces equity claims, retention threats, and recruitment friction over the following two quarters. The on-budget test does not detect band drift because the test is a sum, not a distribution.

A VP of Human Resources at a retail chain described the realization:

"We were on budget at H1 close two years running. The CFO's read was that we had compensation under control. We finally pulled the underlying data and the picture was different. We were on budget because we had higher-than-forecast attrition in two specific role families, which masked higher-than-budget retention adjustments in three others. The aggregate looked clean. The underlying signals were every bit as bad as a meaningful budget overrun would have been, and we were not addressing any of them."

The cumulative cost of running comp on a budget that has drifted from reality has a name worth using: the drift premium. It is the financial weight of decisions made on stale inputs, paid in mishires, missed retention windows, equity remediation, and the slow erosion of internal comp coherence. The premium is rarely a single line item. It is distributed across the year as a series of separate consequences that almost no organization connects back to the original budgeting decision that produced them.

The Reforecast Discipline

The corrective is a quarterly reforecast discipline that tests the budget against current reality on a defined cadence. The reforecast is not a full rebuild — that would be expensive and disruptive. It is a structured checkpoint against the four input categories, with explicit decision rules for when variance demands a budget revision and when it is small enough to absorb.

The reforecast operates on a calendar. Each quarter, four specific reads.

Attrition variance.

Compare actual departures by role family and level against the original forecast. Calculate compensation impact: salary saved from departures, replacement cost at current market rates, retention spend in response to flight risk. The variance number is the gap between budgeted cost and the actual cost of the workforce trajectory the company is on.

Hiring variance.

Compare actual new-hire compensation positions against budgeted positions by role family. Calculate band drift: the average compensation percentile of new hires relative to band midpoint. A persistent drift toward higher percentiles indicates band positions that are below market and need correction; a drift toward lower percentiles indicates a soft labor market for the affected roles or a degraded employer brand.

Merit pool execution.

Track actual merit dollars allocated against budgeted allocation, broken out by performance rating distribution. Variance here surfaces calibration drift — the gap between the distribution the comp committee approved and the distribution managers actually delivered. Persistent inflation of merit allocation against budget signals manager-level rating drift; persistent under-allocation signals performance-system disengagement.

Market positioning.

Refresh against the most recent comp survey data and any meaningful pay transparency signals — public postings for comparable roles, particularly from direct competitors and employers in adjacent geographies. Compare current band positions against current market data. Variance here indicates whether the company's pay structure is keeping pace with the market or falling behind.

The four reads produce four variance numbers. The decision rule is straightforward: when any single variance exceeds an established threshold — typically ten percent of the original budgeted line — or when the aggregate of the four exceeds five percent of total comp budget, the situation triggers a formal reforecast. Below those thresholds, the variance is absorbed and tracked into the next quarter.

This is the reforecast checkpoint: a quarterly governance discipline that tests the budget against reality on a defined cadence and triggers formal revision when reality has moved enough to invalidate the budget's underlying assumptions.

Several advisory firms, Mercer among them, recommend reserving 0.25 to 0.50 percentage points of the total comp budget specifically for mid-year corrections. The reserve funds the adjustments the checkpoint surfaces and removes the budget-friction excuse for ignoring variance signals.

The discipline produces three useful outcomes. It surfaces the silent under-spend, the masking offset, and the band drift before they compound across two more quarters. It creates a defensible decision audit trail — when the comp committee makes a reforecast decision, the inputs are documented and the trade-offs are visible, which matters increasingly in environments where pay equity audits and litigation risk hinge on documented decision-making. And it shifts the governing question from "are we on budget" to "is the budget still right," which is the question that should have been governing comp decisions all along.

What This Requires

Adopting the reforecast discipline requires four organizational changes most companies have not made.

CFO-CHRO Partnership

The first is a CFO-CHRO partnership on quarterly comp reviews. In most organizations, comp planning is a CHRO responsibility and budget governance is a CFO responsibility, with the two functions intersecting at the annual planning cycle and rarely between cycles.

The reforecast checkpoint requires both functions in the room every quarter, with shared data, shared decision authority, and shared accountability for the variance the checkpoint surfaces. This is uncomfortable for organizations whose comp and finance functions have historically operated on separate cadences, and the discomfort is the point — the separate cadences are part of why the drift premium gets paid.

Include Reforecast Authority

The second is a comp committee charter that explicitly includes reforecast authority. Most comp committees are chartered to set the annual comp philosophy, approve the merit pool, and ratify executive comp decisions. Few are explicitly chartered to revise the operating budget mid-cycle.

Adding reforecast authority to the charter formalizes a decision the committee should be making and creates the governance path for action. Without it, reforecast decisions either get made informally — without the deliberation and documentation a formal decision requires — or don't get made at all.

Quarterly Variance Visibility

The third is data infrastructure that surfaces variance on a quarterly cadence. The four reads — attrition, hiring, merit execution, market positioning — require data joined across HRIS, ATS, payroll, and external comp survey sources. Most companies have the underlying data; few have it joined and surfaced as variance reports against budget.

The infrastructure investment is moderate, particularly compared to the drift premium it is designed to detect. The harder challenge is institutional: making variance reports a standard part of quarterly business review, alongside revenue and operating expense, rather than a separate HR analytics product nobody else reads.

Manager-Level Visibility

The fourth is manager-level visibility into actual comp budget against plan, at the role family and team level. Managers making decisions in real time — hiring, off-cycle adjustments, retention conversations — need to see the variance their decisions are creating. Without it, managers default to the assumption that their decisions are budget-neutral, when in fact the cumulative variance from manager-level decisions is the principal driver of the drift the reforecast checkpoint is designed to surface. Visibility produces self-regulation, which is dramatically more efficient than the alternative of governing every manager decision through formal approval workflow.

These four changes do not eliminate budget drift. Drift is structural to the gap between Q4 forecast and H1 reality, and no governance discipline closes that gap entirely. What the changes eliminate is the gap between the drift and the company's awareness of it. A budget that is drifting and tracked is a budget that can be revised. A budget that is drifting and not tracked is a budget that produces six months of compounding suboptimal comp decisions before the year-end reconciliation surfaces what was already true at H1.

The Right Question

The companies that ask whether the budget still represents reality will design comp systems that adapt to a moving market without producing the friction of a continuous rebuild. The companies that keep asking whether they are on budget will arrive at year-end with a clean adherence number and a workforce whose composition, pay, and confidence have all shifted away from the document the number is measuring.