The Manager Premium

The performance gap between your best and worst managers is not a people problem. It is a financial variable, and most organizations are not measuring it like one.

In 2012, researchers at the University of Illinois published a study that quietly reframed how rigorous organizations should think about management investment. Examining twelve years of data from a large service organization, they found that a one-standard-deviation increase in manager quality, moving from an average manager to a good one, produced a performance lift in the manager's team equivalent to adding 1.75 additional employees. They were not adding headcount or capital. They were changing who was doing the managing.

This finding has been replicated in different forms across industries and organizational types. The performance differential between managers in the top quartile of effectiveness and managers in the bottom quartile, when measured against the business outcomes their teams produce, is not a marginal variation. It is a substantial and consistent gap: in revenue generated, quality produced, customer satisfaction achieved, and voluntary attrition absorbed.

Most organizations treat this as a leadership development insight. It is also a capital allocation insight. If manager quality is a financial variable with a measurable return, then the selection, development, and retention of effective managers is an investment with a calculable ROI; one that most organizations have never actually calculated.

Putting Numbers on the Gap

The challenge in quantifying the manager premium is that manager performance is notoriously difficult to isolate. Teams differ in composition, inherited conditions, market territory, and resource access. The manager who looks like a top performer may have inherited a strong team and a favorable market. The manager who looks like an underperformer may be managing through a legacy systems migration and a below-market compensation structure. Controlling for these confounds requires longitudinal data and analytical rigor that most organizations don't apply to people management questions.

When the analysis is done carefully, the numbers are significant. McKinsey research on sales organizations has found that top-performing managers generate 50 percent more revenue per team member than bottom-performing managers in comparable market conditions. Gallup's meta-analytic research across decades of organizational data suggests that manager quality alone accounts for at least 70 percent of the variance in team engagement, which itself drives a 21 percent profitability differential between highly engaged and disengaged business units.

For a team of eight employees with average fully-loaded compensation of $100,000, a $800,000 annual labor investment, the gap between a top-quartile and bottom-quartile manager could represent $150,000 to $250,000 in annual output differential, depending on how the role is defined and how output is measured. This is not speculative; it is a consequence of the engagement, productivity, and retention differences that have been consistently documented between well-managed and poorly-managed teams.

And it compounds. The bottom-quartile manager doesn't just reduce current-year output. They drive voluntary attrition at higher rates than top-quartile managers, creating replacement and vacancy costs that extend the financial impact across multiple years. The average cost of replacing an individual contributor is 50 percent of annual compensation. If a bottom-quartile manager drives two to three additional voluntary exits per year relative to a top-quartile manager, that manager is generating $80,000 to $150,000 in incremental annual recruiting cost before any output differential is counted.

“The same CFO who would immediately model the ROI on a $500,000 technology investment will accept a $2 million annual management performance gap as simply the nature of human variability.”

Why the Measurement Gap Persists

If the financial stakes of management quality are this significant, why do most organizations not measure it with the rigor they apply to other financial variables of comparable magnitude?

Organizational Culture

Part of the answer is organizational culture. Management quality sits in the domain of people, relationships, and leadership, categories that many finance leaders treat as soft and therefore resistant to financial analysis. The same CFO who would immediately model the ROI on a $500,000 technology investment will accept a $2 million annual management performance gap as simply the nature of human variability.

Data Architecture

Part of the answer is data architecture. Organizations typically have good data on what teams produce and poor data on why. Isolating the manager's contribution to team outcomes (separating it from team composition, market conditions, and resource differences) requires analytical investment that most HR functions are not resourced to make.

Accountability Design

Part of the answer is accountability design. In most organizations, managers are evaluated on team output metrics (revenue, productivity, quality) but not on the managerial behaviors that generate those outcomes. They are held accountable for what happened, not for how they managed. This distinction matters because it means that managers who achieve acceptable outputs through poor management practices (high attrition, low engagement, team members developing more slowly than they should) receive adequate performance ratings and continue in their roles without intervention.

The most problematic dynamic is the management-by-output illusion: the organization that believes it is managing management quality because it tracks team performance numbers, while the actual drivers of those numbers (psychological safety, effective feedback, clear expectation-setting, development investment) go unmeasured and unmanaged.

The Cascading Consequences of Bad Management

The financial impact of bottom-quartile management extends well beyond the immediate team. It operates through several reinforcing channels that are worth naming explicitly.

Retention

The retention channel is the most direct. Research consistently identifies the manager relationship as the primary driver of voluntary attrition. The popular formulation, "people don't leave companies, they leave managers," is slightly overstated but directionally accurate. A Gallup study of more than one million employees found that the single largest factor in job dissatisfaction, across industries and geographies, was the quality of the employee's direct manager. Bottom-quartile managers don't just fail to retain their teams; they actively recruit competitors' pipelines by making their employees available.

Development

The development channel is slower but equally significant. Managers are the primary mechanism through which organizations develop their next generation of leadership. Bottom-quartile managers typically do not develop their people, for a combination of reasons, including insecurity about developing potential successors, inadequate coaching skills, and the operational preoccupation that characterizes reactive management styles. The consequence is a talent pipeline that is emptier than it appears on the succession plan, because the nominal high-potentials in poorly managed teams have not received the developmental experiences that would prepare them to step into broader roles.

Engagement

The engagement channel connects manager quality directly to the disengagement liability discussed elsewhere. Bottom-quartile managers are the primary organizational mechanism for converting engaged employees into disengaged ones. They are not doing this intentionally in most cases; they lack the skills or self-awareness to recognize the dynamic. But the financial consequence is the same regardless of intent.

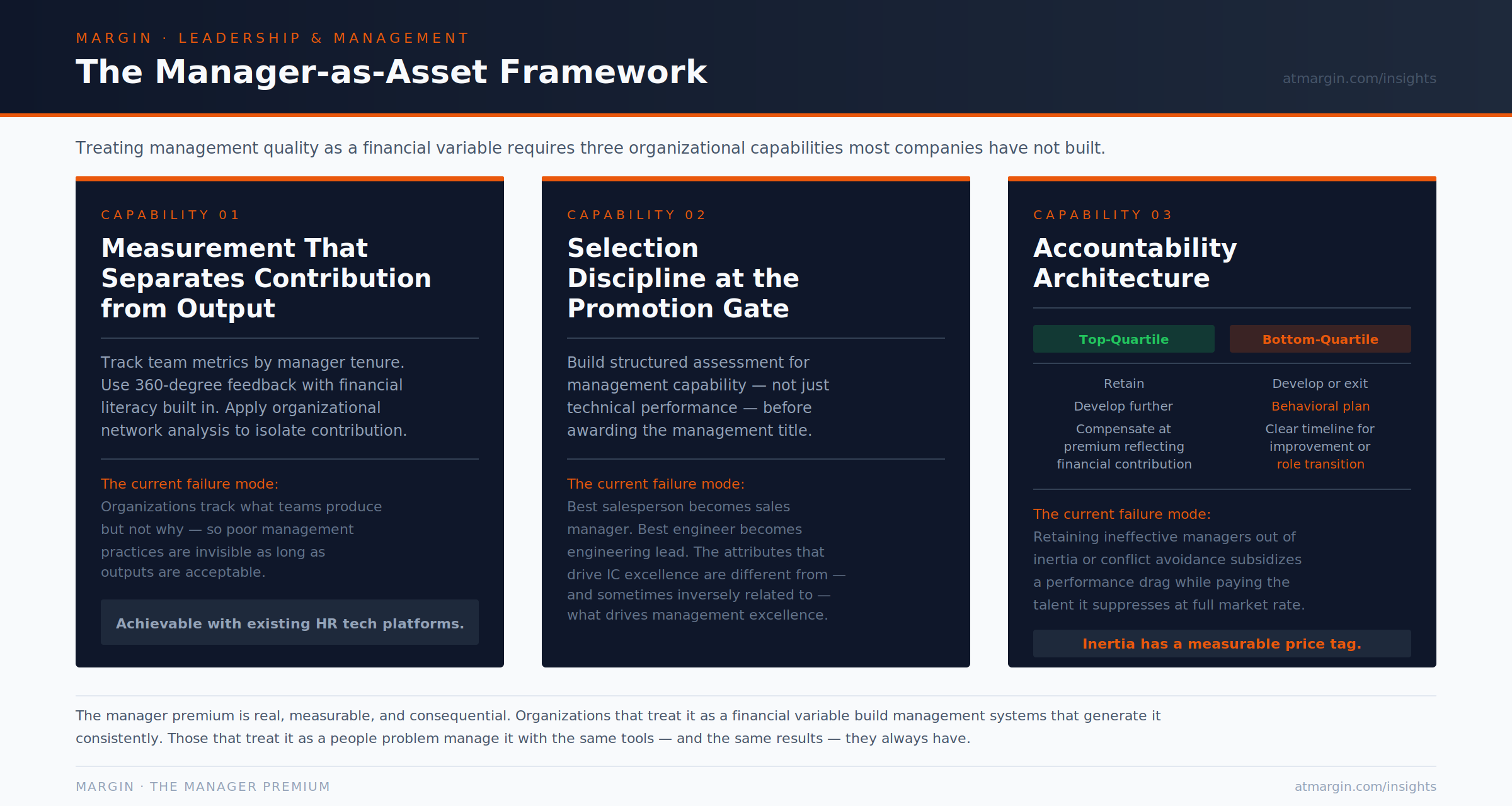

What a Manager-as-Asset Framework Requires

Treating management quality as a financial variable rather than a talent management abstraction requires three organizational capabilities that most companies have not built.

Separate Manager Contribution From Team Output

The first is measurement that separates manager contribution from team output. This requires organizational network analysis, 360-degree feedback with financial literacy built into the instrument design, and longitudinal tracking of team metrics by manager tenure in role. It is not simple work, but it is achievable with existing HR technology platforms for most organizations of moderate scale.

Selection Discipline

The second is selection discipline. The most consequential management quality decision most organizations make is the promotion decision, the choice of who moves from individual contributor to people manager. This decision is made, overwhelmingly, based on technical performance rather than demonstrated management capability. The best salesperson becomes the sales manager. The best engineer becomes the engineering lead. The best analyst becomes the finance manager. The attributes that drive excellence as an individual contributor (domain mastery, competitive drive, technical precision) are different from and in some cases inversely related to the attributes that drive excellence as a manager. Organizations that build structured assessment processes for management capability at the promotion gate, rather than inferring capability from individual performance, make this decision with materially better outcomes.

Accountability Architecture

The third is accountability architecture. Top-quartile managers need to be retained, developed, and compensated in a way that reflects their financial contribution. Bottom-quartile managers need either development plans with behavioral specificity and clear timelines, or transition out of management roles. The organization that retains ineffective managers out of inertia, conflict avoidance, or misplaced loyalty is subsidizing a performance drag while paying the talent that performance drag produces at full market rate.

The manager premium is real, measurable, and consequential. The organizations that treat it as a financial variable will build management systems that generate it consistently. The ones that treat it as a people problem will manage it with the same tools, and the same results, they always have.