Why Q2 Reorgs Destroy Value

The reorg is the most decisive-looking thing a CEO can do, and the most reliably value-destroying. The signal that a reorg is the wrong instrument is exactly the moment most leadership teams reach for it.

Most reorgs are wrong-instrument responses to misdiagnosed problems. The conditions that produce the impulse to reorganize (disappointing Q2 results, board pressure to act, executive frustration with sustained underperformance) are precisely the conditions under which a reorg is structurally unable to fix what it is being deployed to fix.

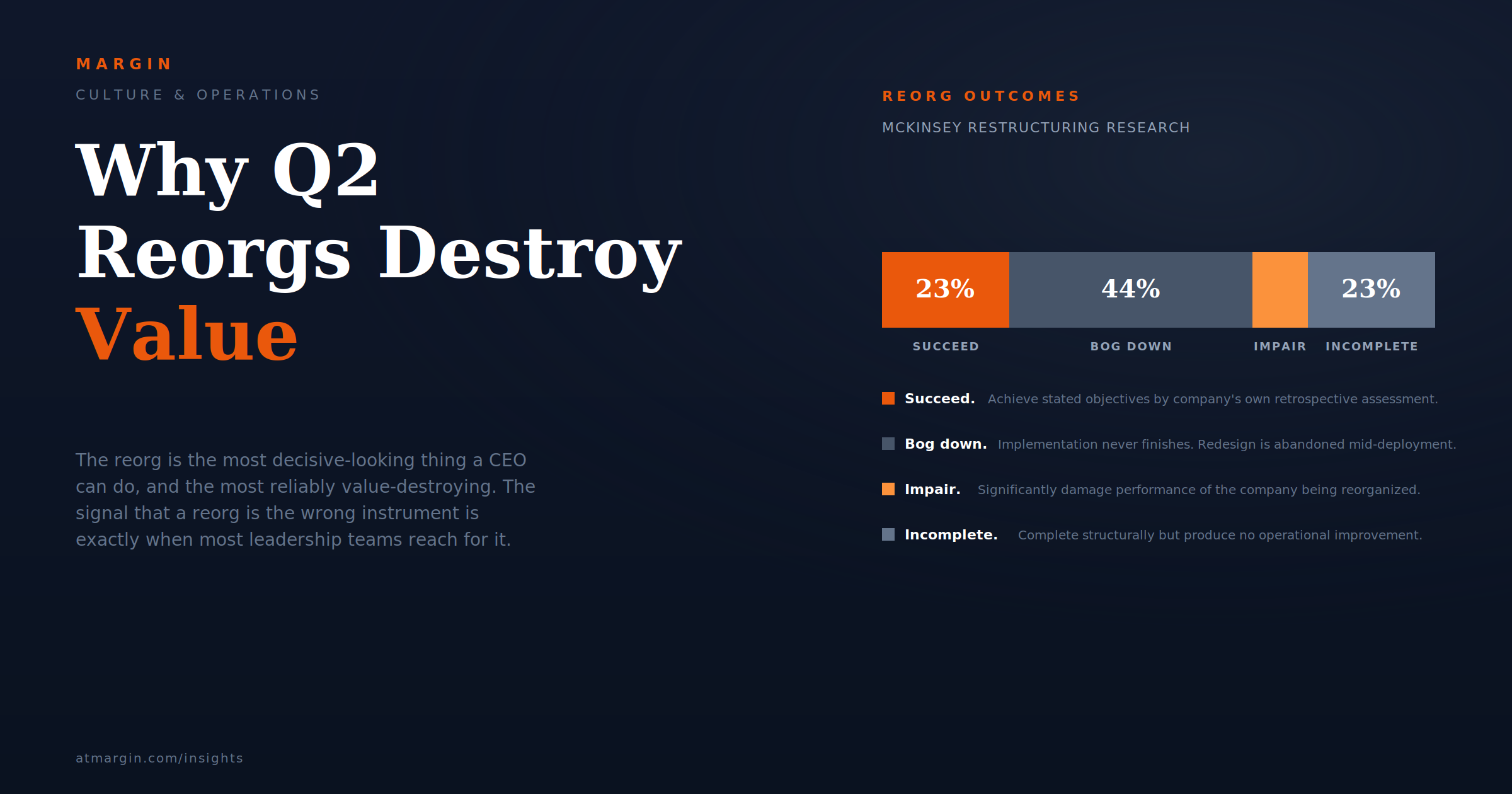

McKinsey's research on the question is unambiguous: only about twenty-three percent of organizational restructurings achieve their stated objectives by their own assessment, over half produce measurable productivity declines during implementation, and the recovery periods routinely extend well beyond initial projections. The minority of reorgs that succeed were doing something the data describes as rare — solving a genuine structural problem with a structural instrument.

The reorgs that follow Q2 results are an especially poor cohort within an already poor population. They arrive on top of whatever structural changes were made at the start of the fiscal year, layering disruption on top of disruption. They are reactive to half-year results that mostly reflect prior-period decisions, not current structure. Their implementation lands in Q3 — the period the reorg is supposed to deliver — and their recovery, if it comes, lands in Q4 or Q1 of the following year, by which point the conditions that prompted the reorg have shifted and a new set of pressures is producing the next impulse. The Q2 reorg is the worst-timed version of a structurally weak instrument, deployed at the moment its weakness will be most amplified.

The cumulative value destruction has a name worth using: the reorg discount — the value the organization absorbs as a one-time write-down on its own operating capacity, paid in productivity loss, knowledge depletion, customer disruption, and the talent attrition that compounds during structural change. The discount rarely appears as a single line item in financial reporting.

It accumulates across multiple quarters as a series of separate consequences, almost none of which the executive team connects back to the reorg that produced them. The reorg that was supposed to deliver clarity becomes the explanation for the next two quarters of underperformance, which produces, in many organizations, the impulse to reorg again.

What the Data Actually Shows

The empirical case against reorgs as a general intervention is consistent across sources and decades of research.

McKinsey's most-cited finding places the success rate of organizational restructurings at approximately twenty-three percent, by the companies' own retrospective assessment. The remaining seventy-seven percent split into two groups: roughly forty-four percent of redesigns bog down during implementation and are never completed, and an additional share — McKinsey estimates around ten percent — significantly impair the performance of the companies the reorgs were meant to revive. The remainder land somewhere between completed and unsuccessful, producing structural change without the operational improvement the change was designed to deliver.

Bain's 2024 analysis of business transformations more broadly placed the failure rate at eighty-eight percent against original ambitions. The gap between the McKinsey figure for organizational reorgs (twenty-three percent success) and the Bain figure for broader transformations (twelve percent success) reflects the different scopes of the studies, but both point to the same conclusion: the structural interventions corporate leaders default to when results disappoint produce, by the strongest available data, predominantly negative or null outcomes.

The productivity dynamics during the implementation period are equally well-documented. Research summarized by Innovative Human Capital and consistent with prior McKinsey findings indicates productivity declines of twenty to thirty percent in the units most affected by a reorg, with knowledge-intensive work particularly vulnerable.

The mechanism is straightforward: established coordination routines are disrupted, working relationships have to be rebuilt, informal work processes get renegotiated, and the social infrastructure that takes months to develop has to be reconstituted before the new structure begins producing the output the old structure was producing. During this rebuild period, total work product declines materially.

The duration of the rebuild is itself longer than most executive teams budget for. McKinsey's research found that a typical reorganization takes approximately ten months from plan to practice. Recovery to pre-reorg productivity adds additional time on top of that — typically another six to twelve months in knowledge-intensive functions, longer in operations and complex multi-site businesses.

The full disruption cycle, in other words, regularly exceeds eighteen months from the moment the reorg is announced to the moment the organization is operating at the level it was operating at before the announcement. The strategic improvement the reorg was meant to deliver has to be evaluated against this baseline; in most cases, the strategic improvement is smaller than the implementation cost when honestly measured.

Indirect costs — productivity loss, knowledge depletion, delayed initiatives, customer disruption, talent attrition — typically exceed direct restructuring expenses (severance, consulting, technology rework) by substantial multiples.

The direct expenses are the part the CFO sees on a line item. The indirect costs are distributed across the operating budget and rarely consolidated into a single number that the executive team can compare against the projected benefits the reorg was sold on.

The Misdiagnosis Underneath the Impulse

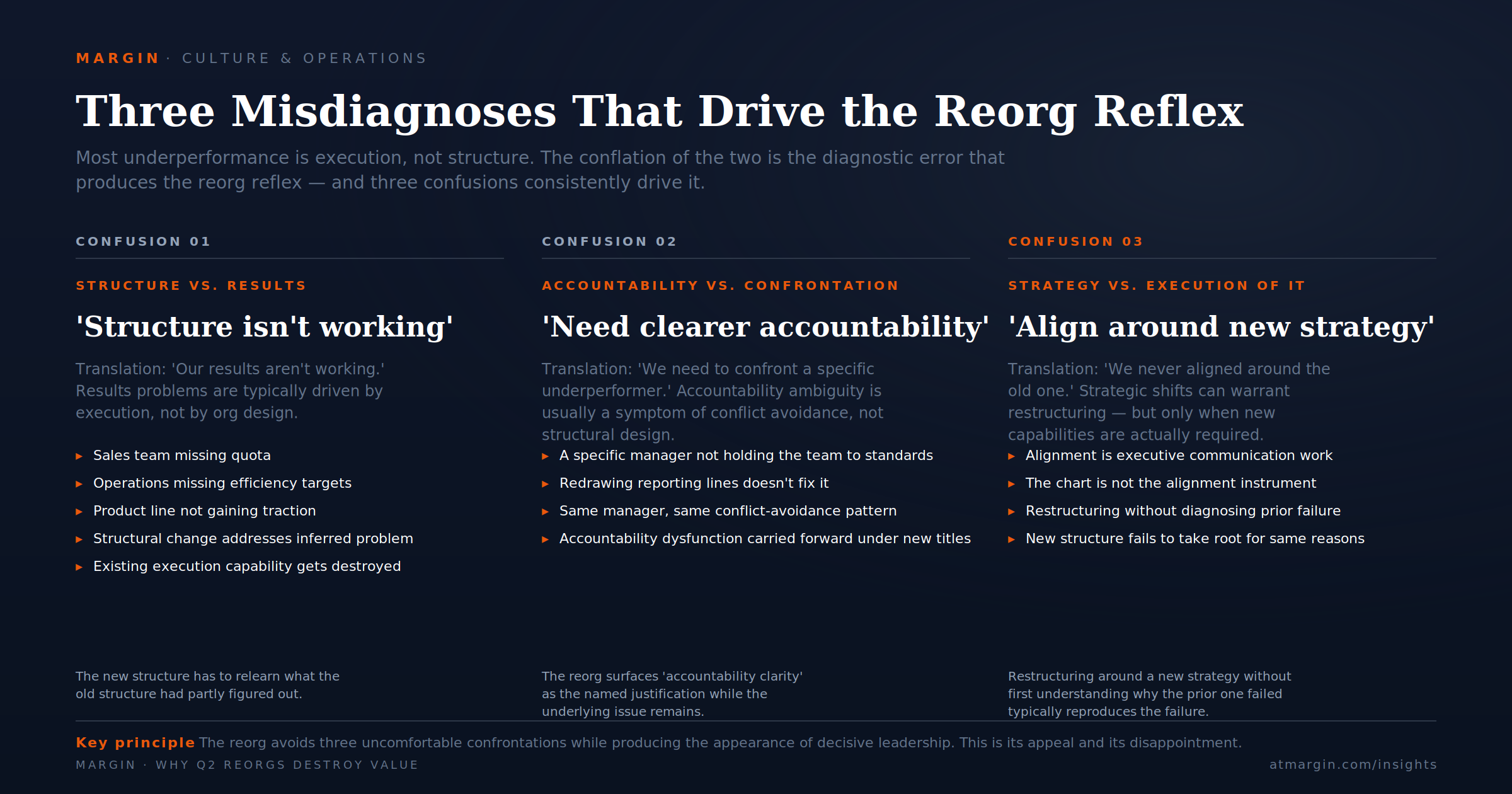

Most reorgs are responses to underperformance. Most underperformance is execution, not structure. The conflation of the two is the diagnostic error that produces the reorg reflex.

“The reorg is the most decisive-looking thing a CEO can do — and the data points to it as the most reliably value-destroying.”

Structural problems are real but rare. They show up as duplicate functions, reporting lines that prevent necessary decisions, and capability mixes that no longer match the strategy. Execution problems are common. They show up as missed deliverables, unclear priorities, undermanaged underperformers, and accountability gaps that exist regardless of what the org chart says.

The two categories produce similar symptoms at the level a senior executive observes — disappointing results, frustrated managers, unclear ownership — but they require different interventions, and the wrong intervention applied to the wrong problem is worse than no intervention at all.

Three patterns of confusion consistently drive the misdiagnosis.

The first is the conflation of "our structure isn't working" with "our results aren't working." Results problems are typically driven by execution: a sales team that isn't hitting quota, an operations team that is missing efficiency targets, a product line that isn't gaining traction.

The structural change that follows — adding a layer of management, splitting the function, merging two teams — does not address the execution problem. It addresses an inferred structural problem that may or may not exist. In the cases where the structure was actually adequate, the reorg destroys the partial execution capability the team had built without producing any replacement. The new structure has to relearn what the old structure had already partly figured out.

The second is the conflation of "we need clearer accountability" with "we need to confront a specific underperformer." Accountability ambiguity is real but is usually a symptom of conflict avoidance, not structural design.

The manager who is not holding their team to standards is the accountability problem; redrawing the reporting lines does not address it because the same manager is in the same role with the same conflict-avoidance pattern. The reorg surfaces "accountability clarity" as the named justification while the underlying issue — that a specific manager is not performing the accountability function the structure already empowered them to perform — remains unresolved. The new structure carries forward the same accountability dysfunction under different titles.

The third is the conflation of "we need to align around the new strategy" with "we never aligned around the old one." Strategic shifts can warrant structural change, but only when the new strategy actually requires capabilities or coordination patterns the existing structure cannot support.

Most "strategic alignment" reorgs are responding to the absence of alignment around the prior strategy — alignment that was the executive team's job to build through communication and execution, not through the organizational chart. Restructuring around a new strategy without first understanding why the prior strategy failed to take root typically produces a new structure that fails to take root for the same reasons.

A CFO at a multi-state facilities services company described the recognition:

"We reorganized three times in four years. Each time the justification was different — alignment, accountability, efficiency, strategy. Each time we promised the board the reorg would produce specific improvements in specific metrics. The metrics moved roughly in line with industry conditions during those four years, which means our reorgs produced approximately zero attributable improvement and absorbed approximately eighteen months of cumulative productivity loss in our largest units. The hardest conversation was admitting that the underlying issue across all three reorgs was the same: we had two regional VPs who were not performing the role the structure already gave them, and we kept rearranging the structure rather than addressing the executives we should have addressed."

The cumulative cost of this pattern is the reorg reflex — the institutional impulse to respond to disappointing results with structural change, regardless of whether structural change addresses the underlying cause. The reflex feels decisive. It is observable from outside the company in ways targeted execution interventions are not.

It allows the executive team to take visible action without making the harder decisions about specific underperformers, unclear priorities, or strategic communication failures. Each of those alternatives requires confronting individuals, sustaining a single coherent narrative for longer than a quarter, or admitting that the strategy itself may not have been clear. The reorg avoids all three confrontations while producing the appearance of decisive leadership. This is its persistent appeal, and the persistent reason it disappoints.

The Reorg Test

The corrective is a diagnostic test applied before any reorg is undertaken: a structured assessment of whether the conditions that genuinely warrant structural intervention are actually present, distinct from the conditions that merely produce the impulse to act.

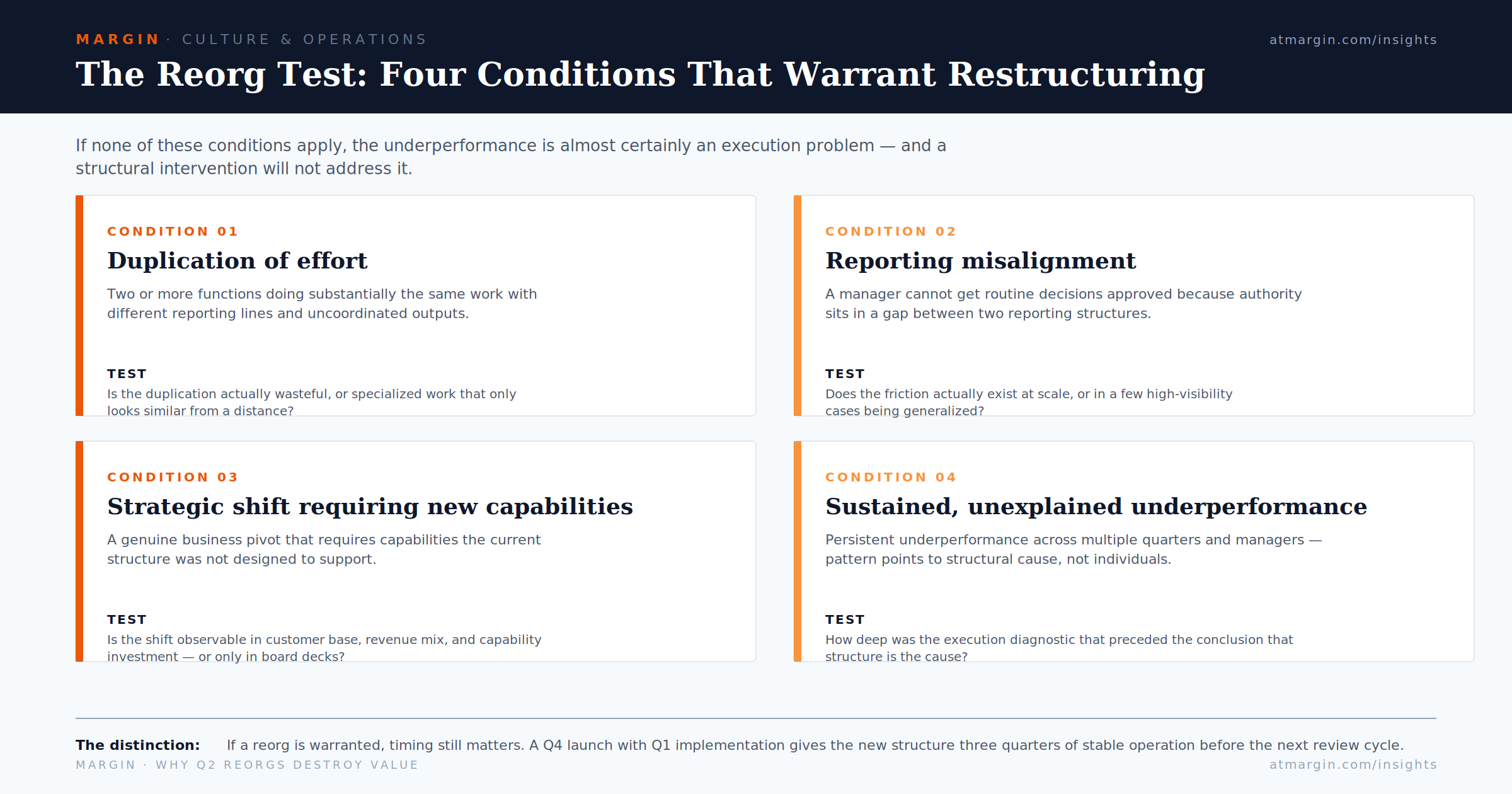

Call this the reorg test. Four conditions are real reorg-warranting situations. The absence of any of them indicates that the underperformance is most likely an execution problem, and that a structural intervention will not address it.

Duplication of effort across functions

When two or more functions are doing substantially the same work, with different reporting lines and uncoordinated outputs, there is a real structural problem and a structural intervention can address it. The test is whether the duplication is actually wasteful (rather than usefully redundant for resilience purposes) and whether merging or restructuring will eliminate it without destroying the partial capability each duplicate function has built. Most companies overestimate the volume of true duplication in their operations. Apparent duplication often turns out, on inspection, to be specialized work that looks similar from a distance.

Reporting misalignment that blocks necessary decisions

When a manager cannot get a routine decision approved because the decision sits in an authority gap between two reporting structures, the structure is producing operational friction that a structural change can resolve. This is the canonical case for a reorg and the one most commonly cited in the justification for change.

The test is whether the friction actually exists at the volume and frequency the reorg case implies, or whether it exists in a small number of high-visibility decisions that are being generalized into a structural argument. The decision-rights diagnostic discussed in companion analyses to this article addresses this question directly: the friction is often resolvable by clarifying decision rights within the existing structure rather than by redrawing the structure itself.

Strategic shift requiring different capability mix

When the company's strategy is shifting in ways that genuinely require a different mix of capabilities — a manufacturer entering services, a distributor adding digital channels, a healthcare network expanding into a new clinical specialty — the existing structure may no longer be aligned to the work the company needs to do.

This warrants structural intervention. The test is whether the strategic shift is real and material, or whether "strategic shift" is being used as a justification for changes the leadership team wants to make for other reasons. Genuine strategic shifts are observable in customer base, revenue mix, and capability investment over multi-year periods. Strategic shifts that exist primarily in board presentations are rarely actual strategic shifts.

Sustained underperformance not explained by execution gaps

When underperformance has persisted across multiple quarters, multiple managers, and multiple execution interventions, and the pattern points to a structural cause rather than to specific individuals or processes, structural intervention may be warranted.

The test is the depth of the diagnostic work that preceded the conclusion. Most "sustained underperformance" reorgs have been preceded by inadequate execution diagnostics — the executive team concluded structure was the issue without seriously testing whether the underperformance was attributable to specific identifiable people or processes that could be addressed individually.

If none of the four conditions apply, the underperformance is almost certainly an execution problem rather than a structural one, and the appropriate intervention is correspondingly smaller. A manager change in a specific function. A role redefinition for a specific incumbent. A process redesign that does not require structural change. A performance management conversation with a specific underperformer.

These interventions are less visible than a reorg, more uncomfortable to execute, and substantially more likely to produce the improvement the reorg was meant to deliver. The discomfort is precisely why the reorg gets reached for instead.

When the test does indicate that a reorg is warranted, timing matters as much as design. A reorg launched in Q2 will absorb implementation during Q3 and recovery during Q4, with the affected units operating at twenty to thirty percent reduced productivity through the period when the original underperformance was already a concern.

A reorg launched in Q4, with implementation in Q1 of the following year, gives the organization three quarters of stable operation under the new structure before the next mid-year review cycle exposes it to the same impatience that produced the initial impulse. The difference in outcome between identical reorgs launched in Q2 versus Q4 is consistently meaningful — and almost entirely a function of the timing decision the executive team made at the moment they decided to act.

What the Restraint Requires

Adopting the reorg test requires four organizational shifts most companies have not made.

The first is CEO discipline against the reorg reflex itself. The impulse to reorg when results disappoint is genuine and pressure-driven; resisting it is uncomfortable because the alternative is visibly slower and less decisive-looking. The CEO has to be willing to absorb the criticism that comes with a less-visible response, to articulate publicly why the diagnostic indicates an execution intervention rather than a structural one, and to hold the line against board or executive team pressure to "do something" in cases where doing the right thing means doing something smaller.

Most CEOs find this discipline harder to maintain than the discipline required to execute a reorg. The reorg gives them something to point to. The execution intervention gives them something to wait through.

The second is honest diagnostic work that distinguishes structure from execution. Most companies skip this step or do it superficially. The diagnostic requires examining specific manager performance, specific process gaps, specific accountability failures, and specific strategic communication breakdowns — and concluding which category the underperformance actually belongs to before concluding what to do about it.

This is the work most executive teams find easiest to defer because it surfaces individual-level performance issues that are uncomfortable to confront. The discomfort is signal: the diagnostic is being avoided precisely because it is producing useful conclusions.

The third is organizational tolerance for slower, more targeted interventions that are less visible to the board and the external market. Execution interventions take longer to produce results than reorgs do, and the intermediate periods are harder to narrate.

The CFO who is asked "what are you doing about the Q2 underperformance" and answers "managing it through specific personnel and process interventions over the next two quarters" has a harder pitch than the CFO who answers "implementing a structural realignment to improve accountability and focus." Both answers may be correct. The first is correct more often and less defensible at the moment of being asked. Building tolerance for the first answer is the cultural work that makes the reorg test sustainable.

The fourth is timing discipline if a reorg does prove warranted. The Q2 launch is structurally worst-timed for reasons the data has consistently shown. A Q4 launch, with implementation in Q1, allows the new structure three quarters of stable operation before the next round of half-year results creates the pressure that produces the next impulse. The timing decision is the difference between a reorg that has a chance to deliver and a reorg that is structurally set up to fail regardless of how well it is designed.

These four shifts do not eliminate reorgs. Genuine structural problems require structural interventions, and the test correctly identifies them when they exist. What the shifts eliminate is the larger share of reorgs — the ones that were responses to misdiagnosed problems, launched at the worst-timed moment, executed against board pressure rather than analytical conclusion, and absorbed as the reorg discount that the organization paid for the appearance of decisive action.

The Reflex and the Cost

The companies that build the reorg test and enforce it will reorganize less often, at better times, against better diagnostics, with materially higher success rates. The companies that don't will keep paying the reorg discount — quarter after quarter, restructuring after restructuring — for the appearance of decisive leadership in moments when the data suggested patience would have produced the better result.