The End of Volatility

In finance, volatility describes fluctuation around a stable mean. When the fluctuation becomes the mean, the term stops applying — and the planning systems most companies still use were designed for an operating environment that has not existed for six years.

In finance, volatility describes fluctuation around a stable mean. The term implies a baseline — a normal state the system returns to once the perturbation passes. When the fluctuation becomes the mean, the term stops applying. The disruptions are no longer disruptions. They are the operating environment.

This is the situation U.S. operating businesses have been in since approximately 2020. Pandemic, supply chain reordering, inflation surge and partial reset, labor market upheaval, AI displacement, tariff cycles, geopolitical reordering, weather-driven operational disruption — these have not arrived in sequence with intervals of stability between them. They have arrived in overlap, with each new disruption beginning before the prior one resolved.

There has not been an eighteen-month window since early 2020 that anyone running a mid-market manufacturer, distributor, healthcare network, or construction services firm would describe as a stable baseline. The financial-modeling concept of "volatility around a mean" has, for practical purposes, stopped describing the world.

Most companies are still planning as if it does. Five-year strategic plans, baseline budgets, normalized headcount forecasts, optimal-when-stable supply chains, contingency reserves treated as exceptional — these are the artifacts of an operating environment in which disruption is the exception. The artifacts have not been updated.

The companies running them are paying the planning tax: the cumulative cost of building plans against a baseline that no longer exists, and absorbing the consequences each time a new disruption invalidates the assumptions the plans were built on.

Their competitors who retired the assumption — who treat continuous adjustment as the operating reality rather than as a transient state to be waited out — are running different systems and producing different outcomes.

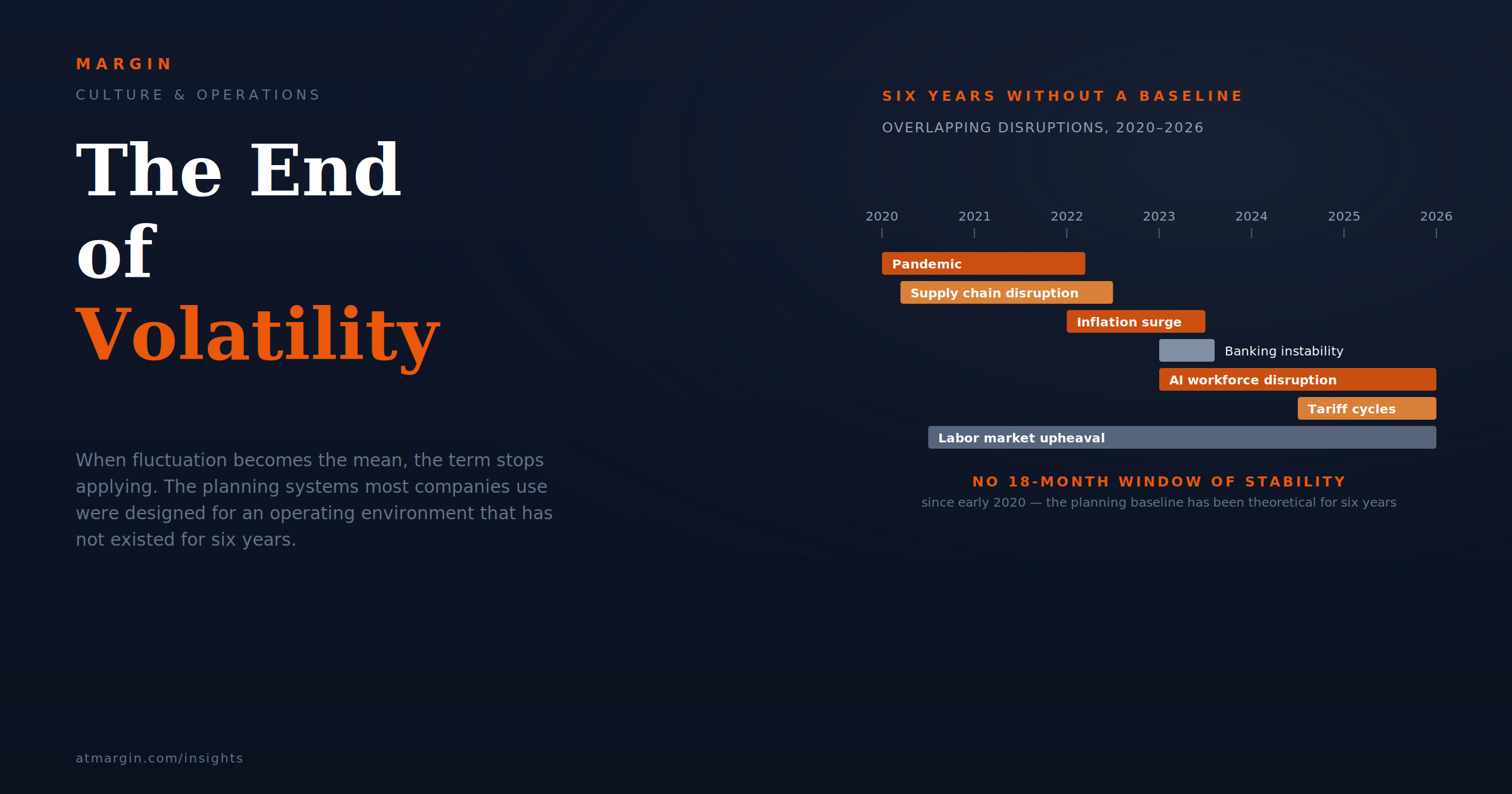

Six Years Without a Baseline

The case for treating volatility as the operating environment rather than as an exception is empirical, not theoretical. Walk the timeline.

In 2020, the pandemic produced simultaneous demand collapse in some sectors and demand surge in others, with a supply chain seizure overlaying both. Companies built plans assuming a six-to-twelve-month return to normal. Most of those plans were obsolete by Q3 2020 and were rebuilt in Q4 against assumptions that were obsolete again by Q1 2021.

In 2021, vaccine rollout coexisted with supply chain disruptions that did not resolve, labor market shifts that did not reverse, and a sustained shift in consumer behavior that defied the "return to normal" assumption planning continued to assume. The Suez Canal blockage was, by historical standards, a black-swan event; in the operating environment of 2021 it was a recognizable incident among several.

In 2022, inflation surged faster than any plan had assumed, the Federal Reserve raised rates at a velocity unmatched in four decades, the Russia-Ukraine war reordered energy and grain markets within weeks, and the labor market reached a tightness that broke compensation models in most industries.

Plans built in late 2021 — when inflation was still being described as transitory — were not approximately wrong; they were structurally wrong, in ways that required full-cycle rebuilds rather than mid-year adjustments.

In 2023, banking instability resurfaced (Silicon Valley Bank, First Republic, Credit Suisse), inflation began cooling unevenly, AI emerged as a workforce question rather than a research curiosity, and labor market dynamics shifted again as some sectors began softening while others remained tight.

The plans rebuilt in early 2023 against the new assumptions were obsolete by mid-year because the underlying environment continued to move.

In 2024, AI accelerated past the curiosity stage into operational deployment, election uncertainty produced a separate planning overlay, supply chain rerouting from China continued to reorder vendor relationships, and several industries faced inflection points in customer behavior that traditional forecasting failed to anticipate.

In 2025 and into 2026, tariff cycles have introduced cost variances that compound across multi-tier supply chains in ways most planning systems were not built to model. Climate-driven operational disruption — weather events, regulatory shifts, insurance market repricing — has continued to add volatility that does not fit neatly into any standard contingency category.

AI maturation has accelerated workforce planning questions that few companies have answered well. Labor market dynamics remain unsettled, with sectoral divergence rather than aggregate clarity.

What this catalog establishes is not that the period has been unusually disruptive. Disruptions occur in every period. What it establishes is that the period has had no intervals of the stability the conventional planning model requires. The model assumes a return-to-baseline that is the precondition for the next plan. The return-to-baseline has not occurred. The model has been operating as if it would, while the operating environment has been operating as if it would not.

The implication is not that volatility is permanent in some metaphysical sense. It is that the conditions of the past six years — overlapping, compounding, multi-vector environmental change — describe the operating environment well enough that planning systems built for any other environment are, on average, wrong.

The companies that continue to plan for the environment they remember from 2018 are not being more conservative than their competitors. They are running on assumptions that have not been true for a longer period than most operating careers ever experience without significant disruption.

What the Planning Tax Looks Like in Practice

The planning tax manifests differently across industries, but the structure is consistent. A plan is built on assumptions about market conditions, input costs, labor availability, regulatory environment, and customer behavior. Each assumption is reasonable at the time it is made. The plan is approved. Within months, one or more of the assumptions becomes obsolete. The company absorbs the variance, either by formal reforecast (rare), by ad hoc adjustment within line items (common), or by accepting the variance as a one-time exception attributable to an unforeseeable event (the most common, and most expensive).

“The variance is not the variance — the variance is the operating environment, and the planning system is still pretending it isn’t.”

In manufacturing, the tax shows up in tariff-driven sourcing whiplash, demand forecasting failures, inventory mispositioning, and capital expenditure decisions calibrated against input prices that have moved by the time the equipment is installed. A capacity expansion budgeted in Q4 against one set of assumptions runs through commissioning against a different set. The company reports the variance in the quarterly review and treats it as exceptional, despite the pattern repeating across each capital cycle.

In distribution, the tax shows up in routing and fuel cost volatility, capacity decisions made against demand forecasts that drift mid-cycle, and labor planning that runs through three different market conditions during a single budget year. The dispatcher who built a route optimization in February cannot run the same optimization in August because the inputs — fuel, driver availability, customer behavior, port and rail conditions — have all moved.

In healthcare, the tax shows up in workforce shortages that planning models continue to treat as cyclical, supply disruption that is now a recurring feature, regulatory shifts that arrive with shorter notice than the budgeting cycle accommodates, and reimbursement environments that change faster than provider pricing can be repositioned. A hospital network that planned headcount in Q4 against an assumed nursing market is operating against a different nursing market in Q2, and the planning artifact has not been updated.

In construction, the tax shows up in commodity price volatility that compounds across multi-year project cycles, labor availability that swings by region and quarter, project delays that propagate through pipeline budgeting, and bid-to-execution intervals during which most of the underlying assumptions become stale. A project priced in spring against one set of input costs is built in fall against a different set, and the gap is absorbed in margin compression that the bid never anticipated.

In retail, the tax shows up in inventory mispositioning against consumer behavior shifts that plans did not anticipate, real estate decisions calibrated against pre-shift assumptions, and labor planning that runs through both wage inflation and store-level availability shifts within a single planning cycle.

In services, the tax shows up in client demand variance that traditional forecasting underweights, labor market shifts that affect both delivery cost and pricing power, and capacity planning that lags the rate at which demand patterns are evolving.

A COO at a regional construction services firm described the recognition:

"We have been treating each year's variances as a one-time disruption. Twenty-twenty-one was the pandemic year. Twenty-twenty-two was the inflation year. Twenty-twenty-three was the labor year. Twenty-twenty-four was the AI year. Twenty-twenty-five was the tariff year. This year is the energy year. We finally laid them out next to each other and asked what the baseline year was supposed to look like. We could not point to one. The variance is not the variance. The variance is the operating environment, and our planning system is still pretending it isn't."

The cost of running this pretense is the planning tax. It is rarely a single line item; it is distributed across reforecast cycles, write-downs, hedging losses, hiring freezes that should have been pipeline expansions, capital projects delayed past the window when they would have been valuable, and the slow erosion of confidence in plans that everyone in the organization has learned not to trust. Most CFOs describe this as variance management. The honest framing is that the underlying planning system is producing fiction, and variance management is the cost of treating the fiction as if it were a plan.

The Volatility-Native Operating Model

The corrective is to redesign the operating systems to assume volatility rather than to wait for stability. The redesign is not a contingency overlay on top of the existing model. It is a different model.

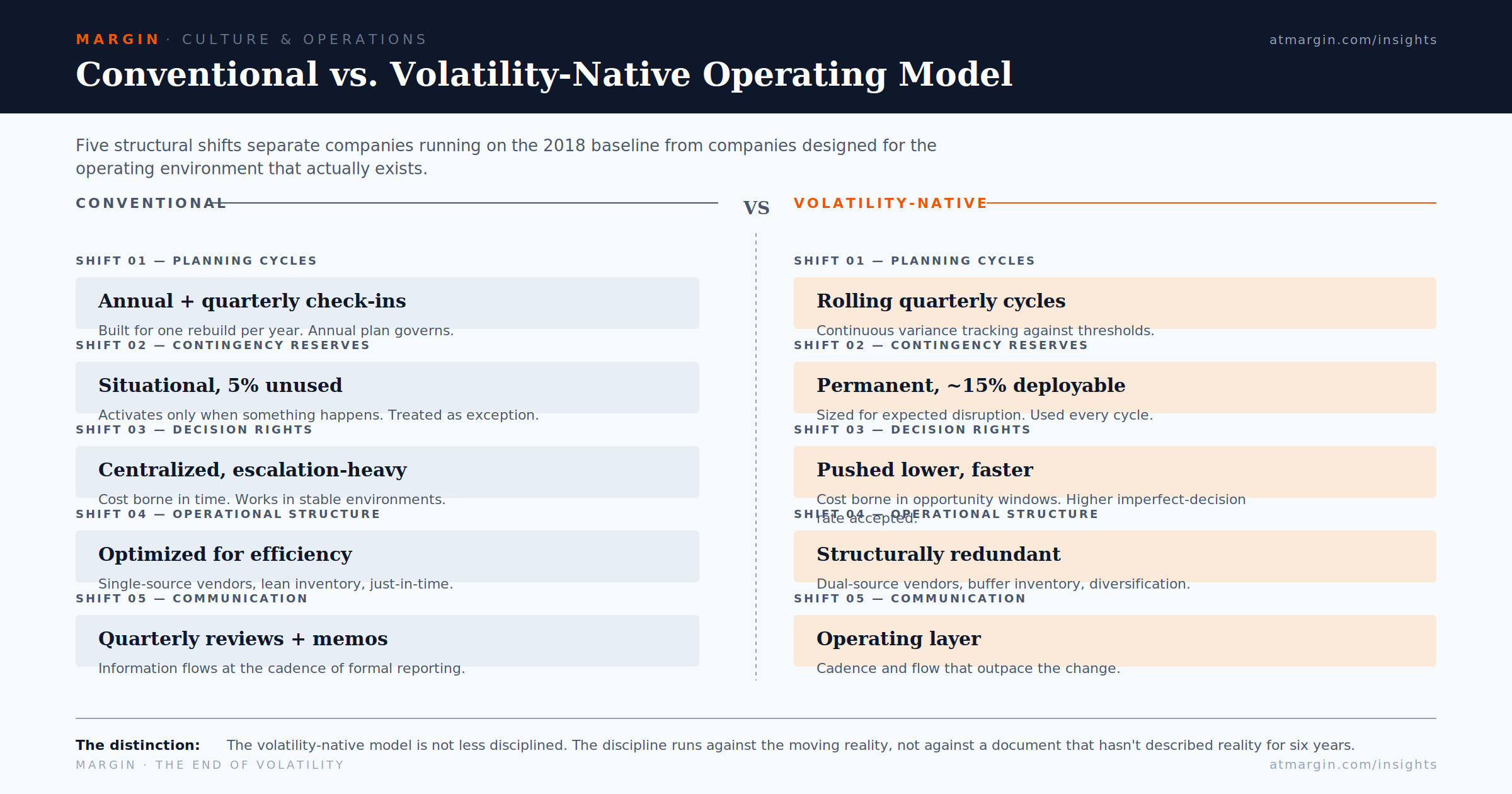

Five shifts define the volatility-native operating model.

Compressed Planning Cyles

The first is compressed planning cycles. The traditional annual budget, supplemented by quarterly check-ins, was designed for an environment in which one rebuild per year was sufficient. In a volatility-native model, planning runs on a rolling quarterly cycle with continuous variance tracking.

The rolling format does not eliminate the annual budget; it complements it with a discipline that accepts the annual document as a point of departure rather than as ground truth. The reforecast checkpoint discussed in previous articles applies here directly: the four input categories that drift in compensation budgets drift in operating budgets too, and the same governance discipline produces better results.

Permanent Contingency Reserves

The second is permanent contingency reserves rather than situational ones. Most companies maintain a contingency line that activates only when something happens. In the volatility-native model, the contingency is permanent, sized against expected disruption rather than against unexpected disruption. The five percent reserve that sits unused for years in the conventional model becomes a fifteen percent reserve that gets deployed every cycle in the volatility-native model.

The total cost is similar; the deployability is structurally different. Companies that have made this shift report that the discipline of treating the reserve as expected, rather than exceptional, changes the planning conversation in ways that affect line decisions across the budget.

Decision Rights Pushed Lower

The third is decision rights pushed lower in the organization. In a stable environment, the cost of escalating decisions is borne in time and senior attention. In a volatile environment, the cost is borne in opportunity windows that close before the escalation completes. The decision rights tax compounds in volatility, because every decision that escalates is a decision that the environment has likely changed by the time the escalation resolves. The volatility-native model pushes decisions to the level closest to the information, accepts the higher rate of imperfect decisions, and recovers the speed-quality correlation that escalation destroys.

Structural Redundancy

The fourth is structural redundancy where traditional efficiency would require optimization. Single-source vendor strategies, lean inventory, just-in-time supply chains, and cost-optimized headcount produced superior margins in the stable environment they were designed for. In the volatility-native environment, they produce fragility — a single disruption in a single input creates downstream consequences that exceed the savings the optimization produced.

The corrective is structural redundancy: dual-source vendor strategies, buffer inventory at strategic nodes, dual-pipeline talent funnels, geographic and supplier diversification that traditional efficiency metrics will mark as waste. The waste, in the volatility-native model, is the cost of resilience. The companies that have made this shift accept lower headline efficiency in exchange for substantially reduced disruption cost across the cycle.

Fast Communication

The fifth is communication infrastructure that operates faster than the conditions change. When the operating environment shifts continuously, the differentiator between organizations is not the plan; the plan is obsolete in any given quarter. The differentiator is the speed at which the organization recognizes that the plan is obsolete and adjusts. Recognition runs through internal communication.

The companies that explain themselves clearly, surface variance quickly, and adjust shared mental models in days rather than quarters operate on a different cycle than the companies that wait for the formal review to surface what has already happened. Communication infrastructure — meeting cadence, dashboard discipline, executive-to-frontline information flow — is the operating layer that determines whether the volatility-native model actually runs or merely exists on paper.

These five shifts together describe an organization that is structurally different from the traditional planning-driven enterprise. It is not less disciplined; the discipline is different. The traditional model exercises discipline against the plan. The volatility-native model exercises discipline against the variance — against the gap between the plan and the present, with formal adjustment processes that close the gap rather than pretend it is not there.

What the Shift Requires

Adopting the volatility-native operating model requires four organizational changes that are uncomfortable in different ways.

The first is CFO acceptance that planning fiction is more expensive than continuous adjustment. Most CFOs were trained in environments where the annual plan was the governance document and variance was a measure of execution quality. The volatility-native model treats the annual plan as a starting point and variance as expected. This is not a small philosophical shift. It implicates how the CFO communicates with the board, how the operating team is held accountable, and how strategic planning is conducted at the executive level. The shift is most often resisted because it appears, from the outside, to weaken financial discipline. The reverse is true: financial discipline in a volatile environment requires discipline against the moving reality, not against the static document.

The second is CHRO redesign of workforce planning around fluid headcount and capability. The traditional headcount plan describes a target end state. The volatility-native model describes a target shape — a distribution of capabilities, scope, and flexibility that adjusts to demand variation rather than holding constant against a fixed forecast. Roles are designed with adjustable scope. Hiring is structured to allow upward and downward adjustment. The compensation system is designed to function across the range of conditions the year is likely to produce, not just the conditions the budget assumed. This requires more sophistication in compensation philosophy and workforce planning than most CHROs have invested in, and most CFOs have funded.

The third is COO investment in redundancy that traditional efficiency metrics will penalize. Operating leaders accustomed to being measured on cost, throughput, and margin face a frank conflict when the volatility-native model asks them to add buffer inventory, dual-source vendors, and reserve capacity that traditional metrics will read as waste. Resolving the conflict requires that the metrics themselves be updated — that the executive team explicitly value resilience as part of operating performance, not as a discount applied during disruption and forgotten between events. Without the metric update, the COO who builds resilience is penalized in normal times and praised in crisis, which is not a sustainable career incentive structure.

The fourth is cultural — comfort with continuous adjustment rather than periodic course correction. The annual planning ritual is a comfort to the organizations that hold it, regardless of whether the resulting plan describes the year that follows. Replacing it with continuous adjustment requires that managers, directors, and executives become comfortable with a different rhythm: shorter horizons, faster revisions, less certainty in any individual quarter, more reliance on judgment than on the plan. This is uncomfortable for organizations whose cultural identity has been built around planning rigor. It is also necessary; the alternative is rigorous adherence to documents that have not described reality for years.

These four changes do not eliminate volatility. Volatility is the environment, and the environment is not subject to corporate decision-making. What the changes eliminate is the gap between the operating environment and the planning system the organization uses to navigate it. In the conventional model, the gap is the source of continuous variance, friction, and missed windows. In the volatility-native model, the gap is the operating discipline — closed continuously, on a cadence that matches the environment rather than fighting it.

The Choice Six Years Late

The companies that recognize the new baseline will design their operations for the world that exists. The companies that don't will keep paying the planning tax — quarter after quarter, disruption after disruption — for a baseline that has not described their operating environment in six years and is unlikely to start.