Bonuses Cause Attrition

The annual bonus is treated as a retention tool. In practice it is the most reliable predictor of when employees who have already decided to leave will actually do so — and the Q1 attrition wave is the bonus working exactly as designed.

A CFO at a mid-market manufacturer signs off on annual bonus payouts in the last week of February. By the second week of April, four senior resignations have crossed her desk — a plant operations director, a senior manufacturing engineer, a regional sales manager, and the controller's number two. The exit interviews are cordial. The reasons are familiar: career growth, manager fit, an attractive market opportunity. They are honest reasons. They are also incomplete. The full reason, the one rarely articulated because it is rarely conscious, is that the bonus payout was the planned execution date for a decision made the previous fall.

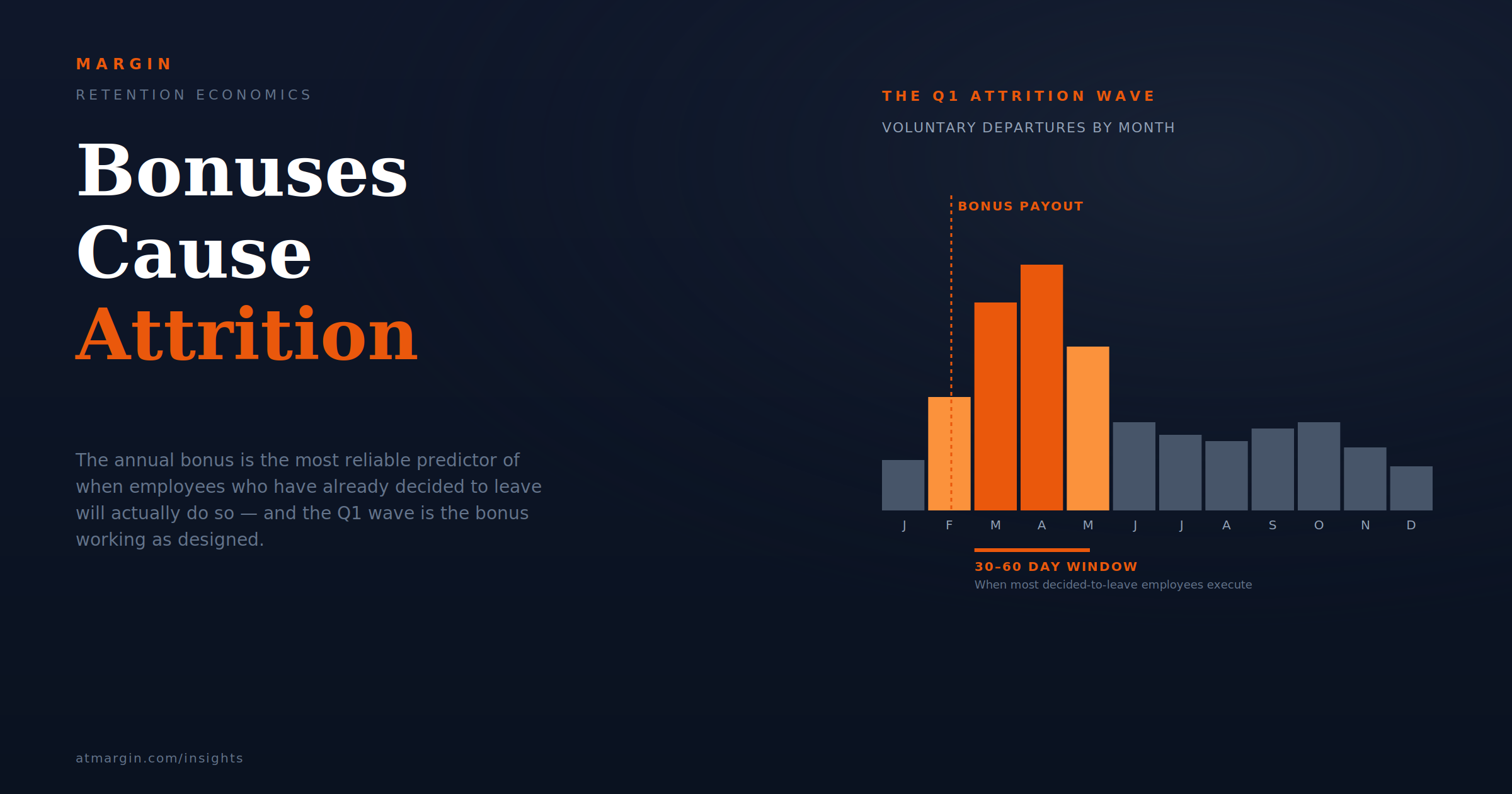

Across the U.S. economy, this pattern repeats every year with metronomic reliability. Annual bonuses pay out between January and March. Resignations cluster February through April. Companies record the wave, attribute it variously to "the job market," "post-pandemic restlessness," or "manager turnover," and then design the following year's bonus pool with no acknowledgment that the bonus structure is producing the wave they are trying to retain against. The instrument designed to keep people pays out at exactly the moment most efficient for leaving them.

This is not a flaw in execution. It is a flaw in framing. An annual bonus is a deferred-compensation contract: stay through year-end and you will be paid for the year. The contract is honored on payout day. From that moment forward, every dollar of future tenure is unpaid for. An employee who has decided to leave loses nothing financially by leaving the day after payout. Most do leave within thirty to sixty days, the time it takes to navigate notice periods and start dates. The Q1 attrition wave is not a culture failure. It is a contract structure executing exactly as designed, on a calendar most companies set themselves.

The Contract Most Companies Don't Realize They Wrote

To understand why annual bonuses produce attrition rather than prevent it, treat the bonus the way a financial analyst would treat any contract: as a series of obligations attached to specific dates.

The annual bonus, structurally, has three parts. The earning period — typically the prior calendar or fiscal year. The performance certification — the manager review and calibration cycle. The payout — the deposit hitting the employee's account, usually between January and March.

"Annual bonus" describes a category rather than a single structure, and the structures vary across the industries this analysis is most relevant to.

Manufacturing and distribution often layer plant or facility performance bonuses on top of individual incentive plans, with different payout timing. Healthcare networks frequently run system-level performance bonuses alongside role-specific incentives. Construction services firms commonly use project-based bonuses that pay on completion rather than against a calendar.

Some industries operate guaranteed bonus structures — 13th-month pay, holiday bonuses — that function as deferred salary and do not produce the wait-and-leave dynamic at all. The analysis that follows applies most directly to performance-based annual bonuses paid as lump sums in Q1, which remain the dominant structure for salaried management roles across most of these industries.

Where alternative structures dominate, the underlying logic still applies — but the specific attrition pattern shifts to follow whatever payout cadence governs the affected workforce.

The earning period and the performance certification are both retrospective. They describe and reward work that has already been done. The employee has worked the year, earned the bonus, and now waits for it to be paid. The waiting period is the only part of the structure that is forward-looking, and it is forward-looking only in a narrow sense: the employee is required to be employed at payout date to receive the funds.

This is the structure of a deferred-compensation contract, and it is well understood in finance. A deferred contract pays out on a fixed date in exchange for performance already delivered, with the only forward-looking obligation being non-departure during the deferral window.

The contract creates exactly one retention force: the cost of forfeiting the deferred amount if the employee leaves before payout. The retention force is real, and it explains why most companies see comparatively few resignations between October and December — the cost of leaving at that point is the loss of an entire year's bonus.

The retention force has an expiration date. On payout day, the deferred amount is paid. From that moment, no future tenure is obligated. The contract has executed. The employee has fulfilled the only forward-looking obligation the bonus structure created, and the structure now exerts zero retention force.

The clean exception to this pattern is a clawback or pro-rated repayment provision: a contractual clause that requires the employee to return some portion of the bonus if they leave within a defined window after payout. Where clawbacks exist, the retention force does extend past payout — typically by six to twelve months.

Clawbacks are standard in executive equity grants, sign-on bonuses, and M&A retention awards. They are uncommon in the annual incentive plans that govern most salaried management roles in mid-market manufacturers, distributors, healthcare networks, retailers, and construction services firms.

Most companies in these industries pay annual bonuses cleanly with no strings attached, which is why the retention force expiration on payout day applies as a general pattern even when specific instruments in the executive comp stack carry longer tails.

This is why post-bonus attrition spikes are not a coincidence and not primarily a market signal. They are the predictable consequence of the only retention force in the bonus structure expiring on a known date. The Q1 attrition wave is the system telling you that the only thing keeping a portion of the workforce in their roles was the unpaid bonus, and the unpaid bonus has now been paid.

What Companies Tell Themselves About the Wave

Most companies that observe the wave attribute it to one of four causes. Each contains some truth. None is the structural cause, and every one of them gets in the way of the analysis that would surface the real driver.

“The instrument designed to keep people pays out at exactly the moment most efficient for leaving them.”

Market Conditions

The first explanation is market conditions. "Hiring picks up in Q1, candidates are getting more offers." This is partially true; Q1 hiring volume generally exceeds Q4. But Q1 hiring activity does not explain why the resignations cluster in the specific weeks after payout rather than spreading across the quarter. The market signal would predict gradual increase. The bonus signal predicts a spike, and a spike is what the data shows.

Manager Turnover

The second explanation is manager turnover. "Our March departures correlate with manager changes the prior fall." Sometimes true. But manager-driven attrition is not seasonal in the way bonus-driven attrition is. Manager turnover produces departures at irregular intervals. Bonus structure produces departures on a calendar.

Compensation Lag

The third explanation is comp lag. "Our compensation is falling behind market and people are leaving for higher offers." Often true. But comp lag predicts a slow, continuous loss of high performers throughout the year, weighted toward those whose market value has grown fastest. It does not predict the synchronized Q1 wave. Comp lag and bonus-cycle attrition are distinct phenomena that get conflated because they both surface as voluntary departures in the dashboard.

Cultural Narratives

The fourth explanation is general post-pandemic restlessness, or generational job-hopping, or whatever cultural narrative is current. These are the explanations companies adopt when the first three don't quite fit. They are diagnostically useless because they imply nothing actionable.

Blaming External Factors

What the four explanations share is that they all locate the cause outside the company's control. The market did it, the managers did it, the candidates' priorities did it.

The structural truth — that the bonus calendar is producing the attrition wave on the calendar the company itself sets — is uncomfortable because it implicates a financial instrument the CFO designed and the comp committee approved. Acknowledging the bonus as the cause means acknowledging that retention and incentive design are coupled in a way most companies have not modeled.

A CHRO at a regional building products distributor described the realization:

"Our voluntary turnover is ten to twelve percent annualized. It looks reasonably good on the dashboard. But four years running, roughly sixty percent of our annual departures have landed between February and April. Two months of the year produce more than half the resignations. We finally stopped pretending it was a hiring market problem and started looking at our own bonus calendar. The wave isn't random."

The cost of the misdiagnosis is significant. The employees who leave in the post-bonus wave are not a random cross-section. They are systematically the highest-performing and most marketable employees — the people with options, the people whose decisions have been forming since the prior fall, the people who timed their search to align with payout.

SHRM places replacement cost at fifty to two hundred percent of annual salary depending on role; in manufacturing specifically, salaried turnover costs run as high as 150 percent of annual salary by published industry estimates.

Compounding the cost, post-bonus departures concentrate in the roles a company can least afford to lose. Call the recurring financial cost of this concentration the payday tax: the structural attrition expense embedded in annual bonus design, paid every spring, rarely modeled, and absorbed by the operating budget as if it were a market condition rather than the consequence of a comp design choice.

Decoupling the Two Things the Bonus Was Asked to Do

The corrective begins with a category distinction most compensation philosophies have collapsed: the difference between compensating past work and retaining future work. The annual bonus does the first job well. It does the second job poorly and at a structural cost.

Compensating past work is what the bonus was designed for: a deferred payment tied to performance, settling at year-end against the employee's contribution to the year's results. This function is intact. The problem is not that bonuses are paid; the problem is that they are asked to perform a retention function that requires a different financial structure.

Retaining future work requires a forward-looking obligation, not a backward-looking settlement. The instruments that actually retain are ones whose value is contingent on continued employment beyond the immediate present: equity vesting schedules with multi-year cliffs, retention bonuses with milestone payments stretched across two or three years, role-based commitments that create value the employee accumulates over time.

WorldatWork survey data places retention bonus structures in the ten to fifteen percent range of base salary for individual contributors and twenty-five to fifty percent for senior or critical-retention roles. None of these instruments replaces the annual bonus. They sit alongside it, creating the forward-looking retention force the bonus does not create.

Call the architecture this implies the retention layer: the set of compensation and non-compensation instruments specifically designed to produce future tenure, distinct from the instruments designed to compensate past work.

A well-designed retention layer for a critical role might include a multi-year retention bonus paid in installments, phantom equity or profit-share vesting on a schedule that extends beyond the next bonus payout, and explicit role-progression commitments tied to milestones rather than calendar dates. None of these instruments individually is novel. The novelty is in treating them as a separately designed system, parallel to but distinct from the annual incentive plan.

For companies and roles that do not warrant retention bonuses or equity, the retention layer takes a different form: a manager investment system. The retention force in a non-equity role comes from the relationship — manager quality, growth opportunity, scope expansion. These are not soft factors. They are the substitutes for financial retention instruments, and they require the same kind of structural investment: manager training, defined growth conversations on a cadence, scope progression tied to performance. The companies that retain non-equity employees do not do so by accident. They do so by treating the retention layer as a system the way they treat the bonus calendar as a system.

The third element of decoupling is timing — using the pre-payout window for active retention conversations rather than waiting for the post-payout wave to materialize. Per the signal stack analysis, the decision to leave forms months before the resignation. The pre-payout window — Q4 of the prior year — is when those decisions are still reversible.

Most companies use Q4 for budget close, performance reviews, and bonus calibration. Almost none use Q4 for explicit retention conversations with high-flight-risk employees. The conversation that happens in November might prevent the resignation that would otherwise arrive in March. The conversation that happens in May, after the resignation, retains nothing.

What the Decoupling Requires

Adopting the retention layer requires four organizational shifts.

Comp Philosophy

The first is a compensation philosophy update that explicitly acknowledges what the annual bonus is and is not. Most comp philosophies still describe the annual bonus as a "performance and retention" instrument, treating the two functions as inseparable. The retention layer treats them as distinct.

The compensation philosophy document should reflect the distinction: the annual bonus rewards prior-year performance; the retention layer produces future tenure; the two are designed and budgeted separately. This is a minor edit on paper and a significant shift in how the comp committee thinks about its role.

Forecasting

The second is a forecast of the post-bonus attrition exposure as a budgeted line item, not a surprise. Most CFOs treat the Q1 wave as a variance against attrition forecasts. Treating it instead as an expected cost — anchored to historical post-bonus departure data — produces several useful effects. It puts the cost on the budget where it can be debated. It creates pressure to reduce the cost through retention layer investment rather than absorbing it. And it forces the comp committee to evaluate the bonus calendar as a financial decision with attached attrition risk, not as a tradition to be honored.

Manager Level Authority

The third is manager-level retention authority during the pre-payout window. Disengagement signals accumulate during the window when interventions are still possible. But interventions require something for the manager to offer — a comp adjustment, a role change, a scope expansion, an explicit growth commitment. Without pre-authorized intervention authority, the manager has nothing to offer the flagged employee except the conversation itself, and the conversation alone, however well-conducted, rarely changes a decision that has been forming since the prior summer.

Staggered Structure

The fourth is a hold-back or staggered structure for the highest-flight-risk roles. For employees in mission-critical roles whose departure would cause meaningful operational disruption, an annual bonus paid in a single February tranche is a structural risk.

Splitting the payout into two or three tranches across the following year, with each tranche conditional on continued employment, transforms the bonus from a backward-looking settlement into a partial forward-looking retention instrument. The total dollars paid are unchanged. The retention force is dramatically increased.

This is uncomfortable for employees who view the annual bonus as fully owed on payout day, and the discomfort is real — which is why hold-backs are typically implemented for senior roles where the flight risk is highest and the operational stakes most material.

Implementation also requires acknowledging a practical constraint: introducing hold-backs retroactively for existing employees is a modification of compensation expectations that may carry employment-contract and reasonable-reliance implications, particularly for employees who have built personal financial commitments around the existing payout structure.

The defensible path is prospective rather than retroactive — introducing hold-backs into new offer structures and into role transitions, and leaving existing comp plans for current incumbents intact until the next natural restructuring point. The slower rollout sacrifices speed in exchange for legal and reputational defensibility, and the trade-off is almost always worth making.

These four shifts do not eliminate the post-bonus attrition wave entirely. Some portion of it is genuinely about market opportunity, manager fit, and other causes the bonus calendar does not produce. What the shifts eliminate is the portion of the wave that exists because the bonus calendar produced it — typically the larger share. Companies that implement the retention layer report measurable reductions in Q1 voluntary turnover, with the reduction concentrated in the high-performing roles where the loss was most expensive.

The Calendar and the Choice

The companies that treat the annual bonus as a retention instrument will keep absorbing the Q1 wave as a market condition they cannot influence. The companies that recognize the bonus as a deferred-compensation contract — and build the retention layer alongside it — will design their compensation calendar as a financial system, not a tradition, and pay the attrition costs they have decided to pay rather than the ones the calendar imposed on them.