The Disengagement Liability

The employees who stay but stop caring represent a larger financial exposure than the ones who quit, and it doesn't appear anywhere on your balance sheet.

The accounting treatment of human capital has always been awkward. People don't appear on the asset side of a balance sheet. Their degraded performance doesn't generate an impairment charge. The slow erosion of organizational output that occurs when a third of your workforce has quietly disengaged from their jobs shows up nowhere in your financial statements: not in cost of goods sold, not in operating expenses, not in any line item that would trigger scrutiny from a board or an activist investor.

This invisibility is not a minor accounting inconvenience. It is a structural blind spot that causes most organizations to systematically misallocate their retention and performance management resources. They spend heavily on replacing the employees who leave. They spend almost nothing measuring or managing the employees who stay but produce materially less than they're capable of.

Gallup's most recent State of the Global Workplace report estimated that low engagement costs the global economy approximately $8.9 trillion annually, roughly 9 percent of global GDP. In the United States specifically, actively disengaged employees (those who are not just checked out but actively undermining organizational performance) represent about 17 percent of the workforce. Another 50 percent are "not engaged," defined as present and minimally productive but not committed to organizational goals. Combined, that is roughly two-thirds of the American workforce operating below full productive capacity.

The turnover conversation, by comparison, is about a much smaller population doing a much more legible thing.

Why Turnover Gets the Attention

The fixation on turnover as the primary metric of workforce health is understandable. Turnover is visible. It generates a transaction: a separation, a backfill requisition, a replacement hire, an invoice from a search firm. It has a cost that can be approximated, even if most organizations approximate it badly. It triggers a response: the exit interview, the counter-offer conversation, the post-mortem about what went wrong.

Disengagement generates none of these signals. The disengaged employee shows up. They respond to emails. They attend meetings. They are, in every operational sense, present. The performance degradation they represent is diffuse and slow-moving, easily attributed to other causes (market conditions, unclear strategy, an underperforming product) rather than traced to the human capital erosion happening inside the organization.

“The engaged employee who watches disengaged peers receive the same compensation and the same advancement opportunities does not simply remain engaged by force of will. They recalibrate.”

There is also a measurement problem. Most organizations measure turnover because they must: the data is generated automatically by the separation process. Measuring engagement requires deliberate effort: designing and deploying surveys, analyzing results, tracking trends over time, and building the organizational will to act on what the data shows. Many organizations do some version of this, but far fewer use the results to construct anything resembling a financial model of their engagement risk.

The result is a resource allocation pattern that is precisely inverted from what the economics would suggest. Replacing a mid-level manager who exits costs between 50 and 200 percent of their annual salary, according to estimates that vary by role complexity and seniority. The ongoing cost of retaining that same manager at 60 percent of their productive capacity, disengaged but present, may be larger in absolute terms when measured over a two-to-three year horizon. Yet the organization invests in the former problem and largely ignores the latter.

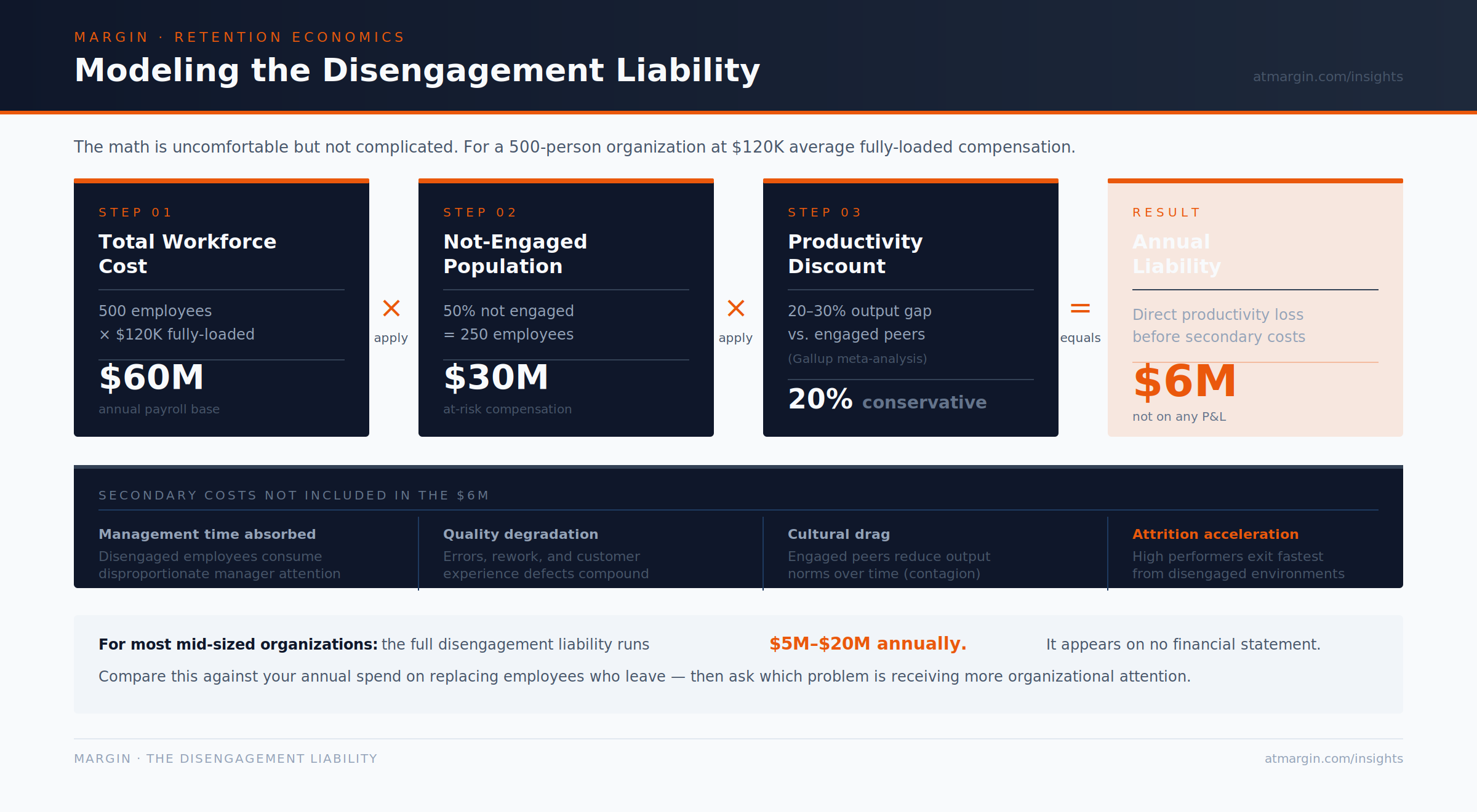

Modeling the Disengagement Liability

For organizations willing to quantify the exposure, the math is uncomfortable but not complicated.

Begin with fully-loaded compensation (salary, benefits, equity, and employer-side taxes) for the roles in question. For a workforce of 500 employees with average fully-loaded compensation of $120,000, total annual workforce cost is $60 million. If 50 percent of that workforce is not engaged, the population in question represents $30 million in annual compensation.

The question becomes: what is the productivity discount associated with disengagement? This is harder to measure precisely, but the research offers useful benchmarks. Highly engaged employees outperform their disengaged counterparts on virtually every business metric: productivity, customer satisfaction, safety, quality, and profitability. The performance differential between engaged and actively disengaged employees, across multiple Gallup studies, is consistently in the range of 20 to 30 percent on measurable output metrics for roles where individual productivity can be tracked.

Applying a conservative 20 percent productivity discount to a $30 million not-engaged workforce cost yields $6 million in annual productivity loss, before accounting for the additional costs of management time absorbed by disengaged employees, the quality defects they introduce, the customer experience degradation they cause, or the cultural drag their presence creates on the engaged employees working alongside them.

This is the disengagement liability. For most mid-sized organizations, it runs between $5 million and $20 million annually. It does not appear on any financial statement.

The Contagion Problem

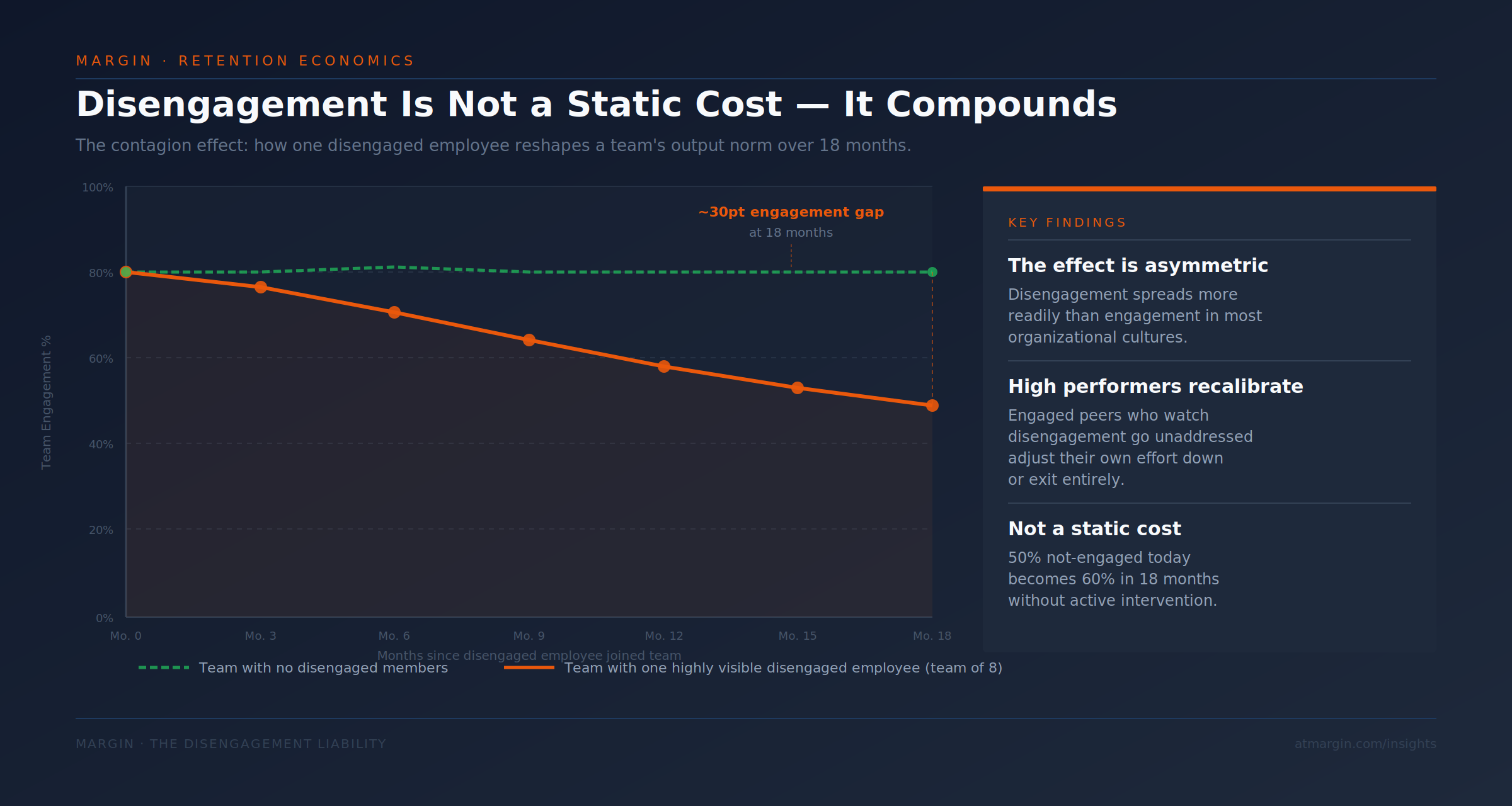

Disengagement compounds in ways that pure turnover does not. An employee who exits takes their negative energy with them. An employee who stays disengaged spreads it.

The social dynamics of organizational disengagement are well-documented. Engaged employees operating in teams with high concentrations of disengaged peers show measurable declines in their own engagement over time. The effect is asymmetric; disengagement spreads more readily than engagement in most organizational cultures. One highly visible disengaged employee in a team of eight can reshape the team's output norm within a matter of months.

This contagion mechanism means that disengagement is not a static cost; it is a growing one. Organizations that do not actively manage engagement risk are not maintaining a steady state. They are permitting a slow degradation of organizational output capacity that compounds year over year. The team that is 50 percent not engaged this year may be 60 percent not engaged in eighteen months, not because anything dramatic happened, but because the social dynamics of low-engagement environments are self-reinforcing.

High performers are not immune to this dynamic. In many cases, they are the most susceptible. The engaged employee who watches disengaged peers receive the same compensation, the same performance reviews, and the same advancement opportunities does not simply remain engaged by force of will. They recalibrate. They begin to ask whether their extra effort is being recognized, rewarded, or even noticed. If the answer is consistently no, they have two options: join the disengaged majority or exit the organization. The organizations that lose their best people fastest to voluntary attrition are often the ones with the highest concentrations of visible disengagement in middle management.

What Finance Leaders Should Be Asking

The disengagement liability belongs in the CFO's portfolio of operational risk measures, not because it is traditionally a finance problem, but because it is a financial problem that has been misassigned to HR and largely ignored.

The questions worth asking are financial in nature. What is our fully-loaded cost per disengaged employee, and how many do we have? What is the estimated productivity discount we are absorbing? What is the annual financial impact, and how does it compare to our turnover cost? What is the trend — is engagement improving or deteriorating? And crucially: what is the ROI of the investments we make in engagement improvement relative to the disengagement cost we are trying to reduce?

Organizations that build an engagement P&L, even a rough one, make better decisions about where to invest in their workforce. They begin to see that the $150,000 employee engagement platform or the $200,000 manager effectiveness training program is not a cost center. It is a lever against a multi-million dollar liability.

The employees who leave show up in the data. The employees who stay and check out never do. But the economics don't care which one triggers a line item.