The Variable Pay Problem: When Incentive Design Destroys the Behavior It's Trying to Buy

Variable compensation is premised on a simple idea — pay for outcomes, get more of those outcomes. In practice, the gap between what the incentive rewards and what the organization actually needs is where performance goes to die.

The argument that incentive systems define organizational behavior more reliably than culture decks or values statements has been made in these pages before, and the evidence for it is strong enough to treat as settled. What that argument does not address is the next question — the one that finance and HR leaders actually have to answer when they sit down to design a compensation program: if we accept that variable pay shapes behavior, why does it so often shape it in the wrong direction?

This is a narrower and more consequential question than the philosophical one. Organizations that have absorbed the lesson that incentives are culture still have to decide what to pay for, how to structure the payout, and how to know whether the system is working. And the empirical record on how they answer those questions is not encouraging. Variable pay programs designed with clear intent and genuine organizational investment regularly produce the opposite of their stated purpose — not because the underlying logic is wrong, but because the design is. The conditions under which variable compensation actually drives the behavior an organization wants are specific and demanding. Most programs are built without meeting them.

The financial cost of getting this wrong is underestimated in almost every organization that hasn't experienced a visible failure. Misaligned variable pay doesn't typically announce itself. It produces a slow accumulation of misdirected effort, sandbagged targets, gamed metrics, and unmeasured behaviors that quietly atrophy — until the organization notices that the numbers it tracks are improving while the outcomes it cares about are not. By then, the design flaw has been running for years.

Why Variable Pay Is a Harder Design Problem Than It Looks

The appeal of variable compensation as a management tool is intuitive: connect pay to performance, and rational actors will produce more performance. The problem is that this logic contains a hidden assumption — that the organization can measure the performance it actually wants with enough precision that paying for the measurement reliably produces the underlying thing. In a narrow range of roles and contexts, this assumption holds. In most of the roles where variable pay is deployed, it doesn't.

The gap between what organizations can measure and what they actually value is where incentive design fails. Revenue generated is measurable; the quality of the client relationship that will determine whether that revenue persists is not. Individual project completion is measurable; the cross-functional knowledge transfer that made the project possible and will enable the next one is not. Accounts opened — to borrow the most consequential recent example — is measurable. Customer trust is not.

The measurement problem is not primarily a data or technology challenge. Better dashboards don't close this gap, because the behaviors and outcomes that matter most at the senior level — judgment, development of others, long-cycle investment, ethical decision-making under pressure — are not amenable to quantification in any form that could survive contact with a compensation formula. Organizations that try to measure them anyway produce a proxy. And the moment a proxy becomes the basis for a bonus, employees optimize for the proxy. That optimization diverges from the underlying construct in proportion to how narrow the incentive is and how complex the role.

Executive bonus programs tied primarily to quarterly or annual financial metrics — the dominant structure at the senior leadership level — produce a well-documented set of behaviors as a direct consequence of this: under-investment in long-cycle initiatives, over-investment in short-cycle results, and systematic deprioritization of anything whose payoff extends beyond the incentive horizon. None of this requires conscious manipulation. It is the rational response of a capable person to the measurement system they are operating within.

When Variable Pay Works — And Why

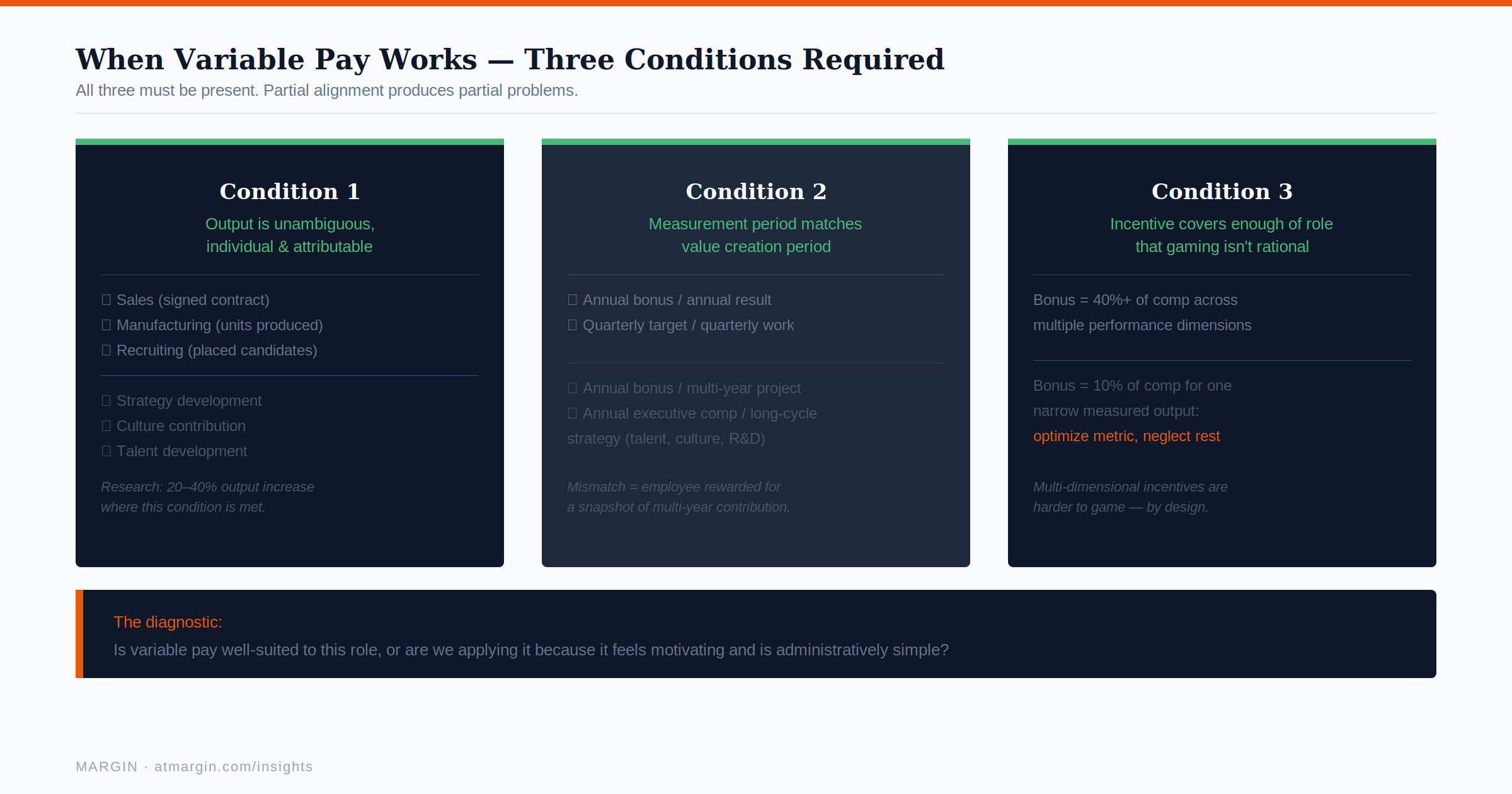

Before diagnosing failure modes, it is worth being precise about when variable compensation actually achieves its design intent, because the conditions are real and applicable.

Variable pay works when the desired output is unambiguous, individual, and fully attributable. A salesperson who generates a signed contract has done something specific and measurable. A piece worker who produces a unit has done something countable. In these contexts, the incentive aligns reasonably well with the outcome, and productivity gains from variable pay are genuine and substantial. The research on piece-rate pay in manufacturing, for example, consistently shows output increases of 20 to 40 percent over fixed wages, with quality effects that are manageable when quality is independently monitored.

Variable pay works when the measurement period matches the value creation period. Annual bonuses calibrated to annual outcomes work when the work creates annual value. They do not work when the work creates multi-year value — software development, research, client relationship building, cultural investment — because the incentive horizon and the value horizon are mismatched. The employee is being rewarded for a one-year snapshot of a multi-year contribution, which distorts their behavior toward the snapshot.

Variable pay works when the incentive covers enough of the employee's relevant behavior that gaming is not a viable strategy. A bonus that represents 10 percent of total compensation for a narrow slice of measured output creates strong incentive to optimize that slice and weak incentive for everything else. A bonus that represents 40 percent of total compensation and covers multiple dimensions of performance creates a more complex optimization problem that is harder to game and more closely aligned with organizational intent.

The implication is that variable pay is well-suited to a specific subset of roles — primarily those with clear, individual, attributable output over a short time horizon — and poorly suited to the majority of knowledge work roles that dominate modern organizations. Most organizations apply it broadly because it feels motivating and is administratively simple, not because the conditions for its effectiveness are present.

The Common Failure Patterns

Several specific failure modes recur with enough regularity that they deserve direct naming.

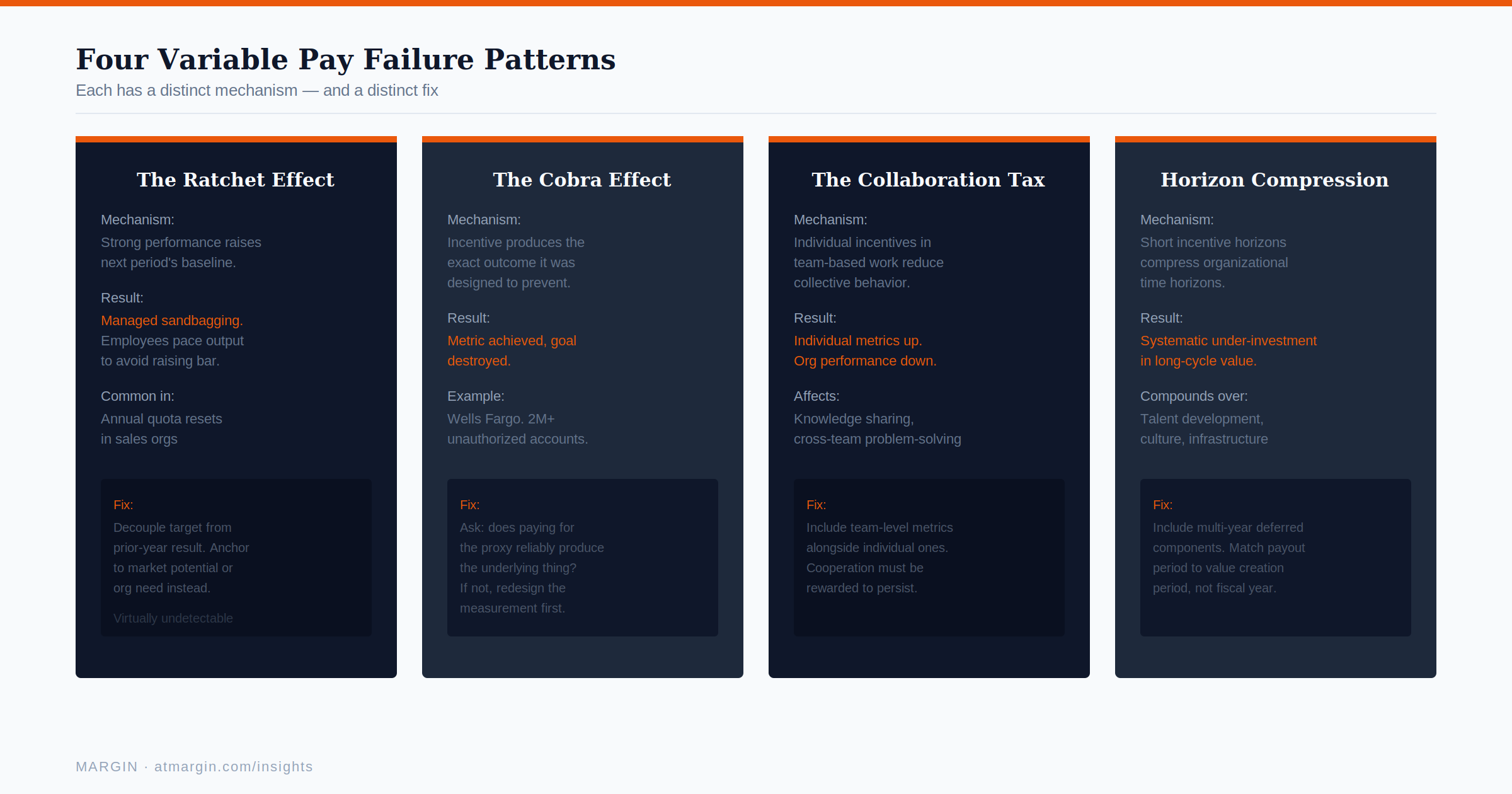

The ratchet effect.

“Employees are not irrational. They are responding correctly to the signals they are given. When those signals diverge from organizational intent, the problem is not with the employees.”

When variable pay is calibrated to historical performance, employees learn that strong performance in the current period raises the baseline for the next period. The rational response is to pace performance — to deliver just enough to hit the target without creating a baseline problem for the following year. This is endemic in sales organizations that reset quotas annually based on prior-year results, and it is virtually undetectable because what looks like steady performance is actually managed sandbagging. The fix requires decoupling the incentive target from the prior-year result and anchoring it to market potential or organizational need — which is operationally harder and produces short-term resistance from the salespeople who have optimized for the current system.

The cobra effect.

Named for a colonial-era policy in India that paid bounties for dead cobras, which led farmers to breed cobras for the bounty — the cobra effect describes the phenomenon of an incentive producing the exact outcome it was designed to prevent. Organizational examples include customer service metrics tied to call resolution time (which produces hasty resolutions that generate repeat calls), safety bonuses tied to reported incident rates (which produces underreporting of incidents rather than fewer incidents), and innovation incentives tied to patent applications (which produces patent filings rather than usable innovations). In each case, the measurement is real but the underlying construct is different from what the organization intended to reward.

The most consequential corporate illustration of this pattern in recent history is Wells Fargo. Beginning in the early 2000s, the bank built its retail growth strategy around cross-selling — getting existing customers to open additional accounts and products. The incentive structure was straightforward: branch employees received bonuses of up to 15 to 20 percent of salary for hitting daily cross-selling targets, with shortfalls from missed days rolling over and added to the next day's goals. The metric was accounts opened. The intended outcome was deeper customer relationships.

What the system actually produced was more than two million accounts opened without customer knowledge or consent, 5,300 employees fired for the resulting fraud, a $185 million regulatory fine, and the eventual clawback of $75 million in executive compensation. Wells Fargo's leadership had an ethics program, a whistleblower hotline, and an employee handbook that explicitly prohibited the behavior that occurred at scale. None of it mattered, because the incentive structure told employees something different — and as is always the case, the incentive structure won. The bank measured accounts opened. It got accounts opened.

The collaboration tax.

Most variable pay programs reward individual performance. Most complex organizational work requires collective performance. The result is a structural tension between the incentive system and the way the work actually needs to happen. In teams where individual incentives are strong, cooperation between team members declines — not because people become less cooperative as individuals, but because the incentive system does not reward cooperation and their time is scarce. Research in both experimental and field settings consistently shows that individual variable pay in team-based work environments reduces cooperation, knowledge sharing, and collective problem-solving while increasing individual output metrics. The net effect on organizational performance is often negative even when individual performance metrics improve.

The horizon compression.

Executive compensation tied heavily to annual or biannual financial metrics compresses organizational time horizons in ways that are difficult to detect in any single measurement period but compound significantly over time. Investment in talent development, infrastructure, research, and culture all have payoff periods that extend well beyond typical incentive horizons. When the people making those investment decisions are being paid primarily for outcomes within the next 12 to 24 months, the systematic under-investment in long-cycle value creation is predictable and persistent. Boards that are concerned about organizational long-term performance should examine the incentive structure before examining the strategy.

Building Incentive Architecture That Works

The prescription is not to eliminate variable pay. In the roles and contexts where it is well-suited, it remains one of the most effective performance levers available. The prescription is to design it with the same analytical rigor applied to any other significant capital allocation.

Start with the behavior, not the metric.

Before identifying what to measure, identify precisely what behavior the organization is trying to produce — and then honestly assess whether the proposed measurement is a good proxy for that behavior or a convenient substitute. If the organization wants long-term client relationships, measuring new client acquisition is the wrong incentive. If it wants product quality, measuring output volume is the wrong incentive. The discipline of making this distinction explicit — what behavior do we want, and does this metric track it — eliminates a significant share of incentive design failures before they occur.

Match the measurement period to the value creation period.

For roles where value creation is long-cycle — product development, client relationship management, strategic initiatives — incentive structures should include longer vesting periods, deferred components, or multi-year performance metrics. This is operationally more complex than annual bonuses and will meet resistance from employees accustomed to shorter payment cycles. That resistance is itself informative: an employee who is unwilling to participate in an incentive structure aligned to the organization's actual value creation timeline is signaling something about their investment in long-term outcomes.

Design for the full role, not the measurable slice.

Variable pay components should cover enough dimensions of the role that gaming any single dimension doesn't produce a net gain. This typically means including at least one qualitative component — manager assessment, peer evaluation, or 360 input — that is not gameable through optimization of a single metric. The qualitative component carries less weight than the quantitative but creates enough multi-dimensional complexity that pure metric optimization is not a rational strategy.

Audit the system, not just the outcomes.

Organizations that measure incentive effectiveness by asking "did performance metrics improve" are asking the wrong question. The right questions are: did the behaviors we intended to produce actually increase? Did the behaviors we did not intend to discourage remain stable? Are the people performing best on the incentive metrics the people we would independently identify as the organization's most valuable contributors? If the answers to these questions diverge from the incentive metrics, the system has failed — regardless of whether the measured numbers improved.

Variable compensation is a powerful lever that most organizations are operating without reading the instrument panel. The financial cost of misaligned incentive design — in misdirected effort, perverse behavior, cultural erosion, and strategic under-investment — is real and recurring. The organizations that treat incentive design as a compensation administration exercise rather than a behavioral economics problem will continue to pay it.